Mastering Capital Budgeting: Your Blueprint for Long-Term Growth

Capital budgeting is a critical financial process that helps businesses evaluate long-term investments and allocate resources efficiently. Whether you’re a small business owner or a financial analyst at a large corporation, understanding capital budgeting is essential for making informed investment decisions. Capital budgeting, often referred to as investment appraisal, is the systematic process by which businesses evaluate and allocate financial resources to long-term projects or assets. It plays a pivotal role in shaping an organization’s strategic direction by determining which investments will generate the highest returns over time. Understanding what capital budgeting entails is essential for anyone involved in financial decision-making, whether you’re managing personal finances or steering a corporation toward sustainable growth.

In this, we’ll cover:

✔ What is capital budgeting? (Definition & Importance)

✔ Types of capital budgeting decisions (Expansion, Replacement, Cost Reduction)

✔ Capital budgeting techniques (NPV, IRR, Payback Period)

✔ Risk analysis methods (Sensitivity, Scenario, Monte Carlo Simulation)

✔ Sources of capital (Debt, Equity, Hybrid Financing)

✔ Tax implications & depreciation

✔ Common mistakes & best practices

Let’s dive in!

Introduction to Capital Budgeting

Definition and Importance

Capital budgeting is the process of evaluating and selecting long-term investments that align with a company’s financial goals. These investments could include:

- Purchasing new machinery

- Expanding operations

- Developing new products

- Acquiring another business

Why is capital budgeting important?

✅ Helps businesses allocate limited resources wisely

✅ Ensures long-term profitability and growth

✅ Reduces financial risks by analyzing potential returns

✅ Supports strategic financial planning

How Capital Budgeting Impacts Long-Term Financial Planning

Capital budgeting decisions shape a company’s financial future. Poor investment choices can lead to:

❌ Wasted capital

❌ Cash flow problems

❌ Reduced competitiveness

On the other hand, smart capital budgeting can:

✔ Improve operational efficiency

✔ Increase shareholder value

✔ Drive sustainable growth

Key Financial Decisions in Capital Budgeting

- Project selection – Choosing the most profitable investments

- Funding strategy – Deciding between debt, equity, or hybrid financing

- Risk assessment – Evaluating potential financial risks

Types of Capital Budgeting Decisions

Certainly! Let’s delve a bit deeper into each type of capital budgeting decision to provide a clearer understanding of their significance, implications, and real-world applications. These decisions are critical for businesses as they directly impact long-term financial health, operational efficiency, and strategic growth.

A. Expansion Decisions

Definition:

Expansion decisions involve investing in new projects or assets to increase the scale of operations, enter new markets, or launch new product lines. These decisions are typically driven by growth strategies aimed at boosting revenue and market share.

Why It Matters:

Expansion decisions are forward-looking and often require significant upfront investment. They carry higher risks but also offer the potential for substantial rewards if executed successfully. Businesses must carefully evaluate whether the expected returns justify the costs and risks involved.

Example:

- A retail chain deciding to open new stores in untapped regions.

- A tech company investing in research and development (R&D) to create innovative products that cater to emerging customer needs.

Key Considerations:

- Market demand: Is there sufficient customer interest to support the expansion?

- Scalability: Can the business handle increased production or service delivery?

- Competition: Will the expansion give the company a competitive edge?

B. Replacement Decisions

Definition:

Replacement decisions focus on upgrading outdated or inefficient equipment, machinery, or technology. These investments aim to maintain or improve operational efficiency, reduce downtime, and lower maintenance costs.

Why It Matters:

While replacement decisions may not directly generate new revenue, they are essential for sustaining productivity and staying competitive. Delaying replacements can lead to higher operational costs, reduced quality, and lost opportunities.

Example:

- A manufacturing firm replacing manual assembly lines with automated robotics to improve speed and precision.

- An IT department upgrading servers to enhance data processing capabilities and cybersecurity.

Key Considerations:

- Cost-benefit analysis: Do the savings from improved efficiency outweigh the cost of replacement?

- Lifespan of assets: How long will the new equipment last, and what is its residual value?

- Technological advancements: Are there newer technologies that could render the replacement obsolete quickly?

C. Cost Reduction Decisions

Definition:

Cost reduction decisions involve investments aimed at lowering operational expenses. These initiatives often focus on improving processes, adopting energy-efficient solutions, or automating repetitive tasks to minimize labor costs.

Why It Matters:

Reducing costs directly impacts profitability, making this type of decision highly attractive. However, businesses must ensure that cost-cutting measures do not compromise quality or customer satisfaction.

Example:

- Installing solar panels to reduce electricity bills and reliance on non-renewable energy sources.

- Implementing enterprise resource planning (ERP) software to streamline workflows and reduce administrative overhead.

Key Considerations:

- Payback period: How quickly will the investment pay for itself through cost savings?

- Long-term benefits: Will the cost reductions sustain over time, or are they short-lived?

- Employee impact: Could automation or process changes lead to workforce disruptions?

D. Regulatory and Mandatory Investments

Definition:

These decisions involve expenditures required to comply with laws, regulations, or industry standards. While these investments may not directly contribute to revenue generation, they are necessary to avoid penalties, legal issues, or reputational damage.

Why It Matters:

Failure to comply with regulatory requirements can result in hefty fines, lawsuits, or even the shutdown of operations. These investments ensure that businesses operate within legal frameworks and maintain their social license to operate.

Example:

- A food processing plant installing advanced sanitation systems to meet health and safety standards.

- A mining company implementing environmental controls to comply with emissions regulations.

Key Considerations:

- Compliance deadlines: When must the investment be completed to avoid penalties?

- Cost allocation: Can the expense be offset by tax incentives or grants?

- Reputational impact: How does compliance enhance the company’s image among stakeholders?

Comparing the Types of Decisions

| Type of Decision | Focus | Risk Level | Return Timeline | Example |

|---|---|---|---|---|

| Expansion Decisions | Growth and market expansion | High | Medium to Long-Term | Building a new factory or launching a new line |

| Replacement Decisions | Efficiency and modernization | Moderate | Short to Medium-Term | Upgrading old machinery with automated systems |

| Cost Reduction Decisions | Lowering operational costs | Low to Moderate | Short-Term | Installing energy-efficient lighting |

| Regulatory Investments | Legal compliance and safety | Low (but mandatory) | Immediate (avoid fines) | Pollution control systems |

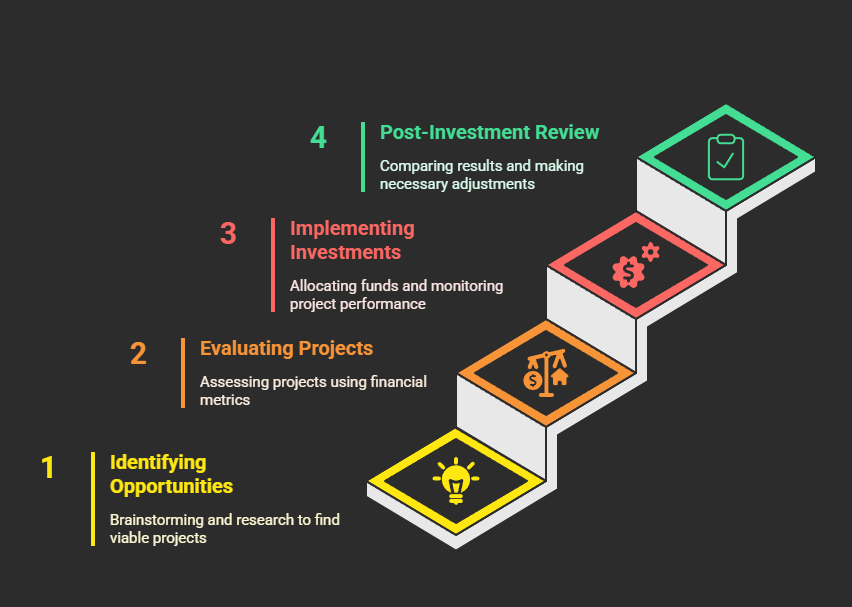

The Capital Budgeting Process

Step 1: Identifying Investment Opportunities

- Brainstorming new projects

- Market research & feasibility studies

Step 2: Evaluating and Selecting Projects

- Using financial metrics (NPV, IRR, Payback Period)

- Comparing different investment options

Step 3: Implementing and Monitoring Investments

- Allocating funds

- Tracking project performance

Step 4: Post-Investment Review and Adjustments

- Comparing actual vs. projected results

- Making necessary adjustments

Capital Budgeting Techniques & Methods

Capital budgeting techniques are essential tools for evaluating the financial viability of long-term projects. These methods provide decision-makers with a structured way to assess whether an investment will generate sufficient returns to justify its costs. Below is a detailed explanation of five widely used capital budgeting techniques:

A. Net Present Value (NPV)

Net Present Value (NPV) is one of the most reliable and comprehensive methods for evaluating investments. It calculates the present value of all future cash inflows generated by a project, discounted at a predetermined rate, and subtracts the initial investment. The formula for NPV is:

NPV = ∑(CFt / (1 + r)^t) − Initial Investment , where CFt represents the cash flow in period t, r is the discount rate, and t is the time period.

The interpretation of NPV is straightforward: if the NPV is positive (NPV > 0), the project is expected to generate more value than its cost, making it a profitable investment. Conversely, if the NPV is negative (NPV < 0), the project is likely to result in a net loss. NPV is highly valued because it accounts for the time value of money, providing a realistic measure of profitability.

B. Internal Rate of Return (IRR)

The Internal Rate of Return (IRR) identifies the discount rate at which the NPV of a project equals zero. In simpler terms, it represents the break-even rate of return for an investment. If the IRR exceeds the required rate of return (or hurdle rate), the project is considered financially viable. For example, if a company’s required rate of return is 10% and the IRR of a project is 15%, the investment is deemed attractive. However, IRR has limitations, such as producing multiple rates in cases of non-conventional cash flows, which can complicate decision-making.

C. Payback Period

The Payback Period measures the time it takes for an investment to recover its initial cost. The formula is:

Payback Period = Initial Investment / Annual Cash Flow .

While this method is simple and easy to understand, it has a significant drawback: it ignores the time value of money and cash flows beyond the payback period. For instance, a project with a short payback period might appear favorable, even if it generates minimal returns afterward. Despite its limitations, the payback period is often used for quick assessments of liquidity and risk.

D. Profitability Index (PI)

The Profitability Index (PI) evaluates the efficiency of an investment by calculating the ratio of the present value of future cash flows to the initial investment. The formula is:

PI = Present Value of Future Cash Flows / Initial Investment .

If the PI is greater than 1, the project is expected to generate more value than its cost, making it profitable. A PI below 1 indicates that the project is unprofitable. PI is particularly useful for ranking projects when resources are limited, as it highlights the return per dollar invested.

E. Discounted Payback Period

The Discounted Payback Period refines the traditional payback method by incorporating the time value of money. It calculates how long it takes for the cumulative discounted cash flows to equal the initial investment. This adjustment makes the method more accurate than the standard payback period but still retains some limitations, such as ignoring cash flows beyond the recovery period.

Each of these techniques offers unique insights into investment decisions, and their combined use ensures a well-rounded evaluation process.

Risk Analysis in Capital Budgeting

Risk analysis is a critical component of capital budgeting , as it helps businesses account for uncertainties and make informed decisions about long-term investments. By incorporating various risk analysis techniques, organizations can better assess the potential outcomes of projects and align them with their risk tolerance. Below is an expanded explanation of key risk analysis methods, using our keywords such as capital budgeting best practices , capital budgeting analysis tools , and what is capital budgeting .

A. Sensitivity Analysis

Definition:

Sensitivity analysis examines how sensitive a project’s financial metrics—such as Net Present Value (NPV) or Internal Rate of Return (IRR) —are to changes in key variables like sales volume, costs, or discount rates. This technique helps identify which variables have the most significant impact on the project’s viability.

Role in Capital Budgeting:

As part of capital budgeting best practices , sensitivity analysis ensures that decision-makers understand the potential risks associated with assumptions in financial models. For example, if a 10% increase in production costs reduces the NPV by 25%, it signals a high level of vulnerability to cost fluctuations.

Example:

A company evaluating a new product launch might test how variations in sales price or raw material costs affect profitability. If the NPV drops below zero under certain conditions, the project may require reevaluation or additional risk mitigation strategies.

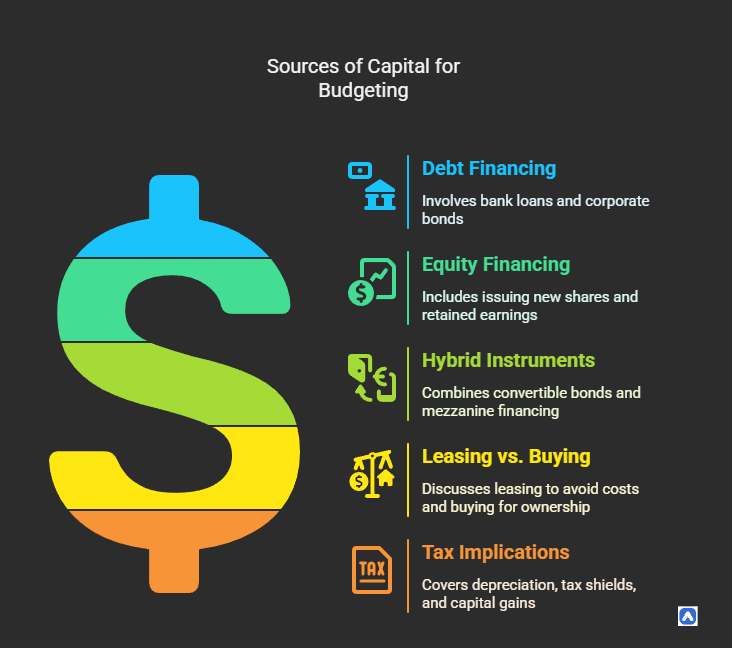

Sources of Capital for Budgeting

7. Tax Implications and Depreciation Considerations

A. Depreciation’s Impact on Cash Flows

- Reduces taxable income

- Increases after-tax cash flow

B. Tax Shields & Incentives

- Accelerated depreciation benefits

- R&D tax credits

C. Capital Gains & Losses

- Tax treatment of asset sales

Capital Budgeting for Small Businesses vs. Large Corporations

| Factor | Small Businesses | Large Corporations |

|---|---|---|

| Budget Size | Limited | Substantial |

| Risk Tolerance | Lower | Higher |

| Decision Speed | Faster | Slower (bureaucracy) |

Common Pitfalls & Mistakes in Capital Budgeting

❌ Underestimating risks & costs

❌ Ignoring inflation & discount rates

❌ Relying on just one evaluation method

Capital Budgeting in the Digital Age

- AI & Machine Learning → Better forecasting

- Financial Software → Faster calculations like axcessRent

- Blockchain → Transparent funding tracking

Conclusion: Capital Budgeting Best Practices

To master capital budgeting , businesses should adopt a disciplined and comprehensive approach that incorporates proven strategies and avoids common pitfalls. Here’s a concise breakdown of the key best practices:

- Use Multiple Evaluation Methods (NPV, IRR, Payback Period):

Relying on a single method can lead to incomplete or misleading conclusions. Combining techniques like Net Present Value (NPV) for profitability, Internal Rate of Return (IRR) for break-even analysis, and Payback Period for liquidity ensures a well-rounded assessment of investment opportunities. - Conduct Thorough Risk Analysis:

Uncertainty is inherent in long-term projects, making risk analysis critical. Techniques such as sensitivity analysis , scenario analysis , and Monte Carlo simulation help identify vulnerabilities and prepare for multiple outcomes. Additionally, using a risk-adjusted discount rate ensures that riskier projects are held to higher return standards. - Consider Tax Benefits & Depreciation:

Tax implications significantly impact cash flows and investment viability. Businesses should account for tax shields from depreciation and explore incentives like tax credits to enhance returns. Properly factoring these elements into financial models can improve the accuracy of capital budgeting decisions. - Avoid Common Mistakes:

Many capital budgeting errors stem from oversight or overconfidence. Avoid underestimating project costs, ignoring inflation, or failing to adjust discount rates for changing market conditions. Similarly, relying solely on simplistic metrics like the payback period without considering time value of money can lead to poor choices.

By adhering to these capital budgeting best practices , businesses can make smarter investments that align with strategic goals, reduce financial risks by anticipating challenges, and ultimately maximize long-term profitability . Whether evaluating expansion projects, upgrading equipment, or complying with regulations, a robust capital budgeting process ensures that resources are allocated efficiently and sustainably.

In essence, mastering what is capital budgeting goes beyond calculations—it’s about fostering a culture of informed decision-making that drives growth and resilience in an ever-changing business environment.

FAQS

What is Net Present Value (NPV), and how is it calculated?

NPV calculates the present value of future cash flows minus the initial investment. The formula is:

NPV = ∑(CFt / (1 + r)^t) − Initial Investment , where CFt is the cash flow, r is the discount rate, and t is the time period. A positive NPV indicates a profitable investment.

What is the Internal Rate of Return (IRR)?

IRR is the discount rate that makes the NPV of a project equal to zero. It represents the break-even rate of return. If the IRR exceeds the required rate of return, the project is considered viable.

What is the Payback Period, and what are its limitations?

The Payback Period measures the time it takes to recover the initial investment. While simple, it ignores the time value of money and cash flows beyond the payback period, making it less accurate for long-term projects.

What is Sensitivity Analysis in capital budgeting?

Sensitivity Analysis tests how changes in key variables (e.g., sales volume, costs) affect a project’s financial metrics like NPV or IRR. It helps identify which variables have the most significant impact on project viability.

What is Monte Carlo Simulation, and why is it used?

Monte Carlo Simulation uses probability distributions to model thousands of potential outcomes for a project. It provides a probabilistic view of possible results, helping businesses quantify risks more accurately.

How can small businesses benefit from capital budgeting?

Small businesses can use capital budgeting to prioritize investments, manage cash flow, and ensure sustainable growth. By adopting simpler methods like the Payback Period and focusing on cost reduction, they can make informed decisions even with limited resources.