What Are Net Assets? A Comprehensive Guide to Financial Success

Net assets serve as one of the most critical indicators in financial reporting, providing a clear picture of an organization’s true financial position. This fundamental accounting concept applies universally across all sectors – from multinational corporations to small nonprofits and government agencies. By examining net asset, stakeholders can evaluate financial health, make informed decisions, and assess long-term sustainability.

What Exactly Are Net Assets?

At its core, net asset represent the residual interest in an organization’s assets after deducting all of its liabilities. This calculation follows the basic accounting equation:

Net Assets = Total Assets – Total Liabilities

This simple formula reveals what would theoretically remain if an organization liquidated all its assets to pay off every outstanding debt. The resulting figure tells us who truly “owns” the remaining value – whether shareholders in a corporation, the public in government entities, or the mission itself in nonprofit organizations.

Key Characteristics of Net Assets:

- For-Profit Context: Known as “shareholders’ equity” or “owner’s equity”

- Nonprofit Context: Referred to specifically as “net assets”

- Government Entities: Often called “net position”

Why Net Assets Matter in Financial Analysis

Net assets serve multiple crucial functions in financial evaluation:

- Solvency Indicator: Positive net assets suggest an organization can meet its obligations, while negative net assets (a deficit) may indicate financial trouble.

- Growth Potential: Organizations with strong net asset positions have more resources to invest in expansion, research, or program development.

- Creditworthiness: Lenders and creditors examine net assets when considering loans or credit terms.

- Investor Confidence: For publicly traded companies, net assets help investors assess the true underlying value of their shares.

- Donor Trust: Nonprofits with healthy net assets demonstrate fiscal responsibility to potential donors.

Net Assets Formula & Calculation

To calculate net assets, you need two key figures: total assets and total liabilities. The formula is straightforward:

Net Assets = Total Assets – Total Liabilities

Let’s break this down step-by-step:

- Identify all assets, including cash, property, equipment, and investments.

- List all liabilities, such as loans, accounts payable, and accrued expenses.

- Subtract the total liabilities from the total assets to arrive at net assets.

Examples of Net Assets Calculation

- Simple Example: A small business has 500,000inassetsand300,000 in liabilities. Its net assets would be 500,000–300,000 = $200,000 .

- Nonprofit Example: A charity holds 1millioninassetsbutowes400,000 in debts. Its net assets are 1million–400,000 = $600,000 .

Types of Net Assets (Nonprofit Context)

In the nonprofit sector, net assets are categorized based on donor restrictions. Understanding these classifications is crucial for financial management and reporting.

| Type | Definition | Usage |

|---|---|---|

| Unrestricted Net Assets | Funds with no donor-imposed restrictions | Can be used for any operational needs |

| Temporarily Restricted Net Assets | Donor-specified use (e.g., “for research only”) | Must be spent per donor terms |

| Permanently Restricted Net Assets | Endowments (principal cannot be spent) | Only investment income is usable |

Unrestricted Net Assets

Unrestricted net assets are funds that a nonprofit can use at its discretion, without any limitations set by donors. These assets offer the organization the most flexibility and are often used for covering general operating costs, launching new programs, or responding to unexpected needs. Since there are no external restrictions, management has the authority to allocate these resources wherever they’re most needed. This category includes revenue from fundraising events, service fees, or general donations that aren’t tied to a specific purpose. For nonprofits, unrestricted net assets are vital for maintaining day-to-day operations and achieving long-term sustainability.

Temporarily Restricted Net Assets

Temporarily restricted net assets are donations or grants given to a nonprofit with specific conditions regarding their use. These restrictions might relate to a time period, such as funds meant for the next fiscal year, or a purpose, like supporting a particular program or event. For example, a donor may contribute $50,000 with the stipulation that it only be used for youth education initiatives. Until the organization fulfills the donor’s conditions, the money remains classified as temporarily restricted. Once the conditions are met—such as spending the funds on the specified program—the assets are reclassified as unrestricted. Managing these assets responsibly is crucial for maintaining donor trust and meeting compliance standards.

Permanently Restricted Net Assets

Permanently restricted net assets are contributions that donors have designated to remain intact indefinitely. Often associated with endowments, the principal of these donations is invested, and only the income or interest earned from those investments can be used for specific purposes. For instance, a donor might contribute $100,000 to establish a scholarship fund, requiring that the original amount be preserved while the earnings support student grants each year. This creates a lasting legacy for the donor and a sustainable funding source for the nonprofit. Managing permanently restricted net assets involves careful investment planning and financial oversight to ensure the principal remains untouched.

Net Assets Released from Restrictions

Net assets released from restrictions refer to funds that were once restricted by donor conditions but have now fulfilled those requirements and are reclassified as unrestricted. This typically happens when a nonprofit spends the money on the designated program, within the required timeframe, or meets the stipulated criteria. For example, if a donor gave $20,000 to fund a summer camp for underprivileged youth, once the camp concludes and the funds are used accordingly, that amount is considered “released.” These reclassifications are important for accurate financial reporting and ensure that stakeholders understand how donor contributions are being used.

Specialized Terms and Related Concepts

Here are some related terms that expand on the concept of net assets:

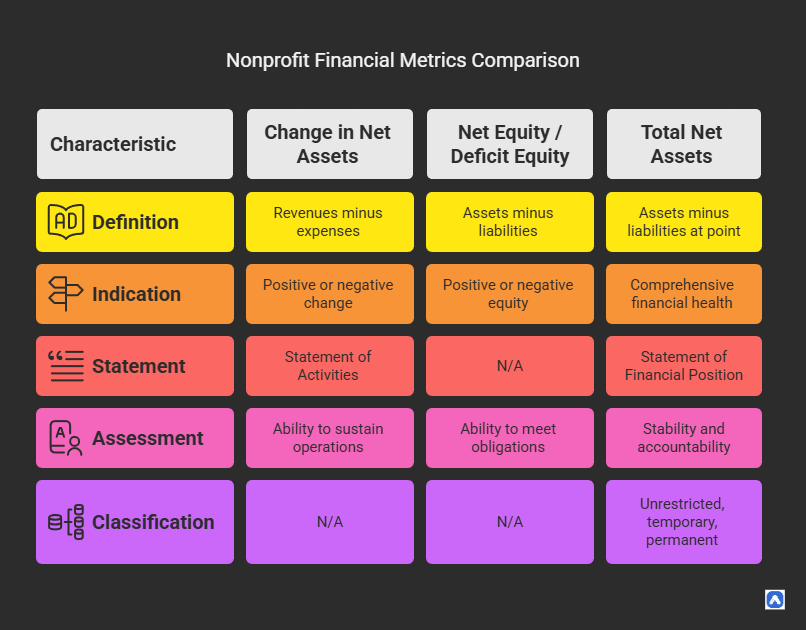

Change in Net Assets

Change in assets measures the financial progress of a nonprofit over a given period. It reflects the difference between total revenues and total expenses, including gains or losses. A positive change indicates financial growth or surplus, while a negative change suggests a deficit. This figure helps stakeholders evaluate the organization’s ability to sustain operations, invest in programs, or expand services. It’s commonly reported in the Statement of Activities and is a key metric in assessing long-term financial health. Monitoring changes in net assets ensures transparency and informs strategic planning and budgeting decisions for future sustainability.

Net Equity / Deficit Equity

Net equity, in the nonprofit context, is similar to net assets and represents the value remaining after liabilities are subtracted from total assets. It reflects the organization’s financial cushion or reserve. A deficit equity occurs when liabilities exceed assets, resulting in negative assets a red flag indicating financial stress or instability. This situation requires immediate attention to restore balance through cost reduction, increased fundraising, or restructuring. Understanding net or deficit equity helps nonprofit leaders and donors assess the organization’s solvency. It’s a vital metric for determining the nonprofit’s ability to meet obligations and continue delivering on its mission.

Total Net Assets

Total net assets represent the overall financial position of a nonprofit at a specific point in time. Found on the Statement of Financial Position (similar to a balance sheet), it is calculated by subtracting total liabilities from total assets. Assets are further classified into unrestricted, temporarily restricted, and permanently restricted categories. This figure provides a comprehensive snapshot of the organization’s financial health and its ability to fund ongoing and future operations. Stakeholders, including donors, board members, and auditors, use this number to gauge the organization’s stability, efficiency, and accountability in managing its financial resources.

Return on Net Assets (RONA)

Return on Net Assets (RONA) is a key financial metric that measures how effectively an organization is utilizing its assets to generate income. It’s calculated using the formula:

RONA = Net Income ÷ Net Assets

For instance, if a nonprofit or business earns $100,000 in net income and holds $500,000 in net asset, the RONA would be 20%. This means the organization is generating 20 cents in profit for every dollar of net asset it owns—a strong indicator of operational efficiency.

RONA is especially valuable for evaluating how well management is using the organization’s resources to produce results. It is often used to benchmark performance against similar organizations or across different time periods. While Return on Assets (ROA) looks at overall asset efficiency and Return on Equity (ROE) focuses on shareholder returns (in for-profits), RONA zeroes in on how effectively an organization’s own equity base is being used to drive financial success.

In the nonprofit world, a strong RONA suggests that donor contributions and internal reserves are being managed responsibly to achieve the organization’s mission.

Applications and Use Cases

Net assets find application in various contexts:

For-Profit Companies

In the for-profit world, net asset often referred to as shareholders’ equity—are a critical measure of a company’s financial strength. Investors and analysts use this metric to evaluate a business’s solvency, growth potential, and overall stability. A positive and growing net asset position suggests that the company has more assets than liabilities, signaling effective management and financial health. It also provides insight into how much value would remain for shareholders if all debts were settled. Companies with strong net asset are better positioned to secure financing, reinvest in operations, and deliver returns to investors through dividends or capital appreciation.

Nonprofit Organizations

For nonprofit organizations, net assets play a vital role in financial transparency and operational planning. Funders, donors, and board members closely examine net asset to ensure the organization is financially sustainable and compliant with donor-imposed restrictions. Net asset are categorized as unrestricted, temporarily restricted, or permanently restricted, allowing stakeholders to understand how funds are allocated and used. A healthy balance of net asset indicates the organization’s ability to support ongoing programs, handle unexpected costs, and invest in future initiatives. By analyzing net asset, leadership can make informed decisions about budgeting, program expansion, and fundraising strategies aligned with their mission.

Government Accounting

In government accounting, net asset reflect the overall financial position of a public entity, such as a municipality, school district, or state agency. These assets are used to demonstrate fiscal responsibility, transparency, and accountability to taxpayers, legislators, and oversight bodies. Public entities must show that they are managing funds efficiently and within budgetary limits. Net asset reporting helps assess whether financial resources are adequate to meet future obligations and support long-term planning. Positive net asset suggest a government is living within its means and managing public resources responsibly, which can enhance public trust and influence funding or policy decisions.

Summary & Key Takeaways

Net assets represent the difference between an organization’s total assets and total liabilities, serving as a key indicator of financial health. This core concept helps determine whether a company or nonprofit is operating within its means. The formula Net Asset = Total Assets – Total Liabilities is simple but powerful, providing insight into solvency and financial stability. In the nonprofit world, net asset are further classified into unrestricted, temporarily restricted, permanently restricted, and those released from restrictions. These categories ensure donor intent is respected and provide a transparent framework for fund allocation, making them essential for ethical and effective financial management.

Beyond understanding the basic definition, key metrics such as Return on Net Assets (RONA) and Change in Net Asset help evaluate performance and operational efficiency over time. A strong RONA indicates efficient use of resources, while an increase in net asset signals financial growth. These insights are crucial across sectors—from nonprofits seeking sustainability to for-profits aiming for profitability. Grasping the concept of net asset enables leaders, investors, donors, and government officials to make informed decisions. Whether planning budgets, fundraising, or assessing long-term viability, net asset remain a foundational tool for measuring success and fostering financial accountability.

FAQs

What are net assets and why are they important?

Net asset represent the difference between an organization’s total assets and total liabilities. They are a critical indicator of financial health, showing how much an entity owns outright. In nonprofits, they demonstrate financial sustainability, while in for-profits, they reflect shareholder equity and solvency.

How do you calculate net assets?

The formula is simple:

Net Assets = Total Assets – Total Liabilities

This calculation helps organizations and stakeholders assess financial stability and resource availability.

What is Return on Net Asset (RONA), and how is it useful?

RONA = Net Income ÷ Net Assets

It measures how efficiently an organization uses its net asset to generate profit or surplus. A higher RONA indicates stronger operational efficiency and effective resource utilization.

How do changes in net assets impact an organization?

An increase in net asset indicates growth or surplus, suggesting the organization is financially sound. A decrease might signal financial strain or a deficit. Tracking these changes helps with planning, budgeting, and strategic development.

How do net assets differ between for-profit and nonprofit organizations?

In for-profits, net asset are similar to equity and reflect ownership value. In nonprofits, they represent the accumulated surplus and are classified based on donor restrictions. Both sectors use net asset to gauge financial strength, but the context and reporting vary.

What does a negative net asset (or deficit equity) mean?

A negative net asset position means liabilities exceed assets—commonly known as deficit equity. This indicates financial risk and the need for corrective actions like reducing expenses, restructuring debt, or increasing funding.

How do organizations use net assets for planning and decision-making?

Net assets guide decisions in budgeting, expansion, fundraising, and borrowing. Positive net assets improve credibility and allow organizations to invest in growth, meet obligations, and weather financial challenges effectively.

How are assets and liabilities connected to net worth?

Assets and liabilities are the building blocks of net worth. The relationship is defined by the formula:

Net Worth (or Net Assets) = Total Assets – Total Liabilities.

Assets include everything the organization owns—such as cash, property, and equipment—while liabilities are what it owes, like loans or payables. A higher amount of assets compared to liabilities results in positive net worth, indicating financial strength. Conversely, if liabilities exceed assets, the organization has a negative net worth (also called a deficit), which could be a warning sign of financial instability. This formula is essential for understanding an entity’s true financial position.