How to Tackle Outstanding Debt: Proven Strategies for Faster Repayment

What is Outstanding debt ?

Outstanding debt refers to any amount of money that is owed but has not yet been repaid. It encompasses a wide range of financial obligations, from personal loans and credit card balances to unpaid business invoices and government bonds. Understanding outstanding debts is crucial—not just for maintaining financial stability but also for making informed decisions about borrowing, spending, and long-term financial planning.

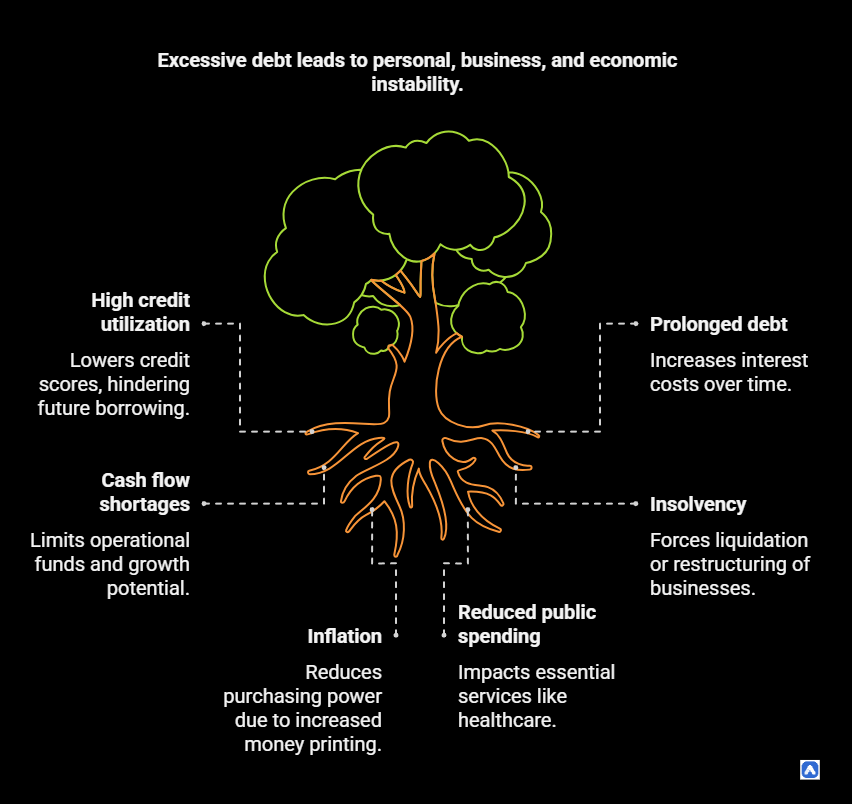

For individuals, mismanaged debt can lead to high-interest payments, damaged credit scores, and even bankruptcy. For businesses, excessive outstanding debts can strain cash flow, harm supplier relationships, and threaten solvency. On a macroeconomic level, national debt influences inflation, interest rates, and economic policy. Given its far-reaching implications, learning how to track, manage, and reduce outstanding debt is an essential skill for financial health.

Types of Outstanding Debt

Debt comes in many forms, each with its own terms, risks, and repayment structures. Broadly, outstanding debts can be categorized into three main types: consumer debt, business debt, and government debt.

Consumer Debt

This includes any money owed by individuals for personal expenses. Common examples are:

- Credit card balances – Often high-interest and revolving, meaning they carry over if not paid in full.

- Personal loans – Fixed-term loans used for various purposes, such as home improvements or emergencies.

- Mortgages – Long-term loans secured by real estate, typically with lower interest rates.

- Auto loans – Financing for vehicle purchases, usually with fixed repayment schedules.

- Student loans – Debt taken for education, which may have flexible repayment options.

Business Debt

Companies take on debt to fund operations, expansion, or cash flow needs. Forms of business debt include:

- Vendor payments – Unpaid invoices owed to suppliers (accounts payable).

- Business loans – Term loans or lines of credit from banks or alternative lenders.

- Corporate bonds – Debt securities issued to investors for capital.

Government Debt

Governments borrow money through instruments like:

- Treasury bills (T-bills) – Short-term securities maturing in less than a year.

- Government bonds – Long-term debt used to fund infrastructure and public services.

Each type of debt carries different risks and repayment expectations, influencing how individuals and organizations should approach their liabilities.

How Outstanding Debt is Recorded

Debt is an inevitable part of both personal and business financial landscapes. Whether it’s a mortgage, a student loan, or a corporate bond issuance, understanding how it is recorded is critical for maintaining financial health. The way debt is documented varies depending on the context personal finances versus business operations but the underlying principles remain consistent: clarity, accuracy, and transparency are key.

Personal Debt Tracking

In personal finance, outstanding debt often appears in documents like bank statements and credit reports, which serve as primary tools for tracking financial obligations. These statements act as a practical reminder of what you owe and help you stay on top of payment deadlines. Credit reports, meanwhile, offer a broader perspective by summarizing your borrowing history, including current debts and past behaviors like late payments or defaults. This information is particularly critical because it directly impacts your credit score, which lenders use to assess your reliability when considering new loans or credit applications.

Individuals can monitor their outstanding debts through:

- Bank statements – Show loan balances and credit card dues.

- Credit reports – Provide a comprehensive view of all debts, including payment history and creditor details.

Business Debt Accounting

When it comes to businesses, outstanding debt is meticulously documented on the balance sheet, a key financial statement that provides a snapshot of a company’s financial position. On the balance sheet, debt is categorized under the “Liabilities” section, which is further divided into two distinct categories: current liabilities and long-term liabilities. This division allows businesses to prioritize their short-term cash flow needs while also planning for future obligations. By organizing debt in this way, companies can better assess their financial health and make informed decisions about investments, expansions, or cost-cutting measures.

On a company’s balance sheet, outstanding debts appears under liabilities, split into:

- Current liabilities – Debts due within a year (e.g., accounts payable, short-term loans).

- Long-term liabilities – Obligations due beyond a year (e.g., mortgages, corporate bonds).

Key accounting terms include:

- Gross outstanding debt – The total amount owed before accounting for repayments.

- Net debt – Gross debt minus cash reserves.

Causes of Outstanding Debts

Debt accumulates for various reasons, ranging from strategic borrowing to financial mismanagement.

Planned Borrowing

Not all debt is a result of financial struggles; some borrowing is intentional and strategic. Mortgages are a prime example, as they allow individuals to invest in homeownership, which often appreciates over time. Similarly, businesses may take on loans to fund expansion projects, purchase equipment, or hire additional staff, with the expectation that these investments will generate future revenue. In such cases, debt serves as a tool for growth and long-term value creation. While planned borrowing carries risks, it is typically managed carefully, with repayment schedules aligned to the borrower’s ability to meet obligations. When used wisely, this type of debt can lay the foundation for financial stability and prosperity.

Some debt is intentional, such as:

- Mortgages for homeownership – A long-term investment.

- Business expansion loans – Used to scale operations.

Unplanned Expenses

Unforeseen circumstances can quickly lead to debt when individuals face expenses they cannot cover out of pocket. Medical emergencies often top the list, as high healthcare costs not covered by insurance can force people to rely on credit cards or loans. Similarly, sudden car or home repairs—like a broken engine or a leaking roof can create urgent financial demands. These unplanned expenses disrupt budgets and push individuals into borrowing cycles, even if they previously managed their finances responsibly. Without an emergency fund to fall back on, many find themselves turning to high-interest credit options, making repayment more challenging over time.

Unexpected costs can force borrowing, including:

- Medical emergencies – High bills not covered by insurance.

- Car or home repairs – Sudden breakdowns requiring immediate payment.

Poor Financial Management

Debt can also stem from habits like overspending, failing to budget, or relying heavily on credit. Impulse purchases, lifestyle inflation, and the misuse of credit cards often lead to mounting balances that become difficult to repay. High-interest rates on credit card debt exacerbate the problem, causing balances to grow faster than payments can reduce them. A lack of financial literacy or discipline may prevent individuals from recognizing the long-term consequences of their spending decisions. Over time, poor financial management creates a cycle of dependency on borrowing, leaving individuals struggling to regain control of their finances and achieve stability.

- Overspending, lack of budgeting, and high-interest borrowing can lead to unsustainable debt levels.

Economic Factors

Macroeconomic conditions play a significant role in shaping borrowing patterns and repayment challenges. Rising inflation can erode purchasing power, forcing individuals to borrow more to cover basic expenses. During recessions, job losses or reduced income can make it harder to meet existing debt obligations. Additionally, rising interest rates increase the cost of borrowing, making loans and credit card payments more expensive. These factors disproportionately affect those already burdened by debt, creating a ripple effect that worsens financial strain. Even disciplined borrowers may find themselves struggling under the weight of economic pressures beyond their control, highlighting how external forces can amplify personal financial challenges.

Risks of Outstanding Debt

Personal Risks

Carrying excessive debt can have serious consequences for individuals, starting with its impact on credit scores. High credit utilization and missed payments signal financial instability to lenders, leading to lower credit ratings. This, in turn, makes it harder to secure loans or credit cards with favorable terms. Additionally, prolonged debt often results in higher interest costs, as borrowers pay more over time due to compounding rates. In severe cases, overwhelming debt may push individuals toward bankruptcy—a legal process that discharges debts but leaves long-lasting damage to creditworthiness and financial reputation. These risks highlight the importance of managing personal debt responsibly to avoid spiraling into financial distress.

- Lower credit scores – High credit utilization and missed payments hurt ratings.

- Higher interest costs – Prolonged debt leads to more interest paid over time.

- Bankruptcy – Severe cases may require legal debt discharge.

Business Risks

For businesses, excessive debt can strain operations and jeopardize sustainability. High levels of borrowing may lead to cash flow shortages, leaving companies unable to cover daily expenses like payroll or inventory purchases. This lack of liquidity can stifle growth and erode investor confidence. In extreme cases, insolvency becomes a real threat, where the inability to meet financial obligations forces liquidation or restructuring. Over-leveraged companies also face challenges in securing additional funding, as lenders perceive them as high-risk. These risks underscore the need for prudent financial planning and disciplined borrowing practices to maintain operational stability and long-term viability.

- Cash flow shortages – Too much debt can choke operational funds.

- Insolvency – Inability to meet obligations may force liquidation.

Economic Risks

Excessive national debt poses significant risks to a country’s financial health. Large debt burdens can lead to inflation as governments print money to meet obligations, reducing the purchasing power of citizens. To manage debt, governments may cut public spending on essential services like healthcare and education, impacting societal well-being. Alternatively, higher taxes may be imposed to generate revenue, placing additional strain on households and businesses. These measures can slow economic growth, increase unemployment, and create widespread financial instability. Managing national debt is therefore critical to ensuring sustainable development and avoiding adverse effects on the broader economy.

Managing and Reducing Outstanding Debt

Effectively managing and reducing outstanding debts requires a structured approach, starting with a thorough assessment of your financial situation. Begin by listing all debts, including their amounts, interest rates, and due dates. This clear overview helps prioritize which debts to tackle first and ensures no obligations are overlooked. When it comes to payment strategies, two popular methods can be particularly effective. The snowball method focuses on paying off the smallest debts first, providing psychological wins that build momentum. Alternatively, the avalanche method targets high-interest debts to minimize long-term costs, saving money on interest payments.

Assessment

Assessing your debt is the first step toward regaining financial control. Start by listing all debts, including their amounts, interest rates, and due dates. This comprehensive overview helps you understand the scope of your obligations and prioritize repayments effectively. Knowing which debts carry the highest costs or are due soon allows you to allocate resources strategically. A clear assessment also prevents missed payments, which can harm credit scores and increase financial strain. This foundational step ensures a targeted and organized approach to debt management.

Payment Strategies

The snowball method focuses on paying off the smallest debts first while maintaining minimum payments on others. This approach builds motivation through quick wins, as eliminating smaller balances creates a sense of accomplishment. On the other hand, the avalanche method targets high-interest debts first, minimizing the total interest paid over time. While it requires more patience, this strategy saves money in the long run. Choosing the right method depends on your financial goals and whether you value psychological boosts or cost efficiency.

- Snowball method – Pay smallest debts first for psychological wins.

- Avalanche method – Target high-interest debt to save money long-term.

Budgeting & Negotiation

Budgeting is essential for freeing up funds to tackle debt. Cutting unnecessary expenses, such as dining out or subscriptions, redirects money toward repayment. Additionally, negotiating with creditors for lower interest rates can reduce overall costs, making it easier to pay down balances faster. Consolidation loans are another option, combining multiple debts into one payment with a lower rate. These strategies not only simplify finances but also create a sustainable path to debt reduction by aligning spending with repayment priorities.

Professional Help

When debt becomes overwhelming, professional help can provide guidance and structure. Credit counseling agencies offer advice on budgeting and debt management, helping individuals create realistic repayment plans. Debt management programs may consolidate debts into a single monthly payment with reduced interest rates. These services are designed to alleviate stress and prevent further financial damage. By working with experts, individuals gain access to tools and strategies tailored to their unique situations, paving the way toward long-term financial stability and peace of mind.

Outstanding Debt and Credit Scores

Outstanding debts plays a significant role in determining your credit score, which influences your ability to secure loans or credit in the future. Key factors include the credit utilization ratio, which measures the percentage of available credit you’re using. High utilization, especially on credit cards and revolving debt, signals financial strain and can lower your score. Payment history is equally critical; missed or late payments negatively impact your score and stay on your credit report for years. A high ratio suggests over-leveraging, making it harder to qualify for favorable terms.

Impact of Late Payments and Defaults

Late payments and defaults have severe consequences for your financial health. Even a single missed payment can significantly lower your credit score, as it indicates unreliability to lenders. Defaults, which occur when debts remain unpaid for extended periods, are even more damaging and may lead to collections or legal action. These negative marks can linger on your credit report for up to seven years, making it challenging to rebuild your financial reputation. Avoiding late payments through careful budgeting and prioritizing debt repayment is crucial to maintaining a healthy credit profile.

Strategies to Improve Credit While in Debt

Improving your credit score while managing debt requires a proactive approach. Start by paying bills on time, as consistent payment history positively impacts your score. Focus on reducing high-interest revolving debt, like credit card balances, to lower your credit utilization ratio. Consider setting up automatic payments to avoid missing deadlines. If possible, negotiate with creditors to restructure payments or reduce interest rates. For those overwhelmed, enrolling in a debt management plan through credit counseling can help consolidate debts and ensure timely payments. These strategies not only improve your credit score but also create a sustainable path toward financial recovery.

Legal and Regulatory Aspects of Outstanding Debt

When dealing with outstanding debts, understanding the legal and regulatory framework is essential to protect your rights and navigate potential challenges. These laws not only safeguard consumers but also provide structured options for managing overwhelming debt. Below are key aspects of debt-related legal protections and regulations:

Consumer Protections

Several federal laws are designed to protect borrowers from unfair practices by lenders and debt collectors:

- Fair Debt Collection Practices Act (FDCPA): This law restricts how debt collectors can communicate with consumers. It prohibits harassment, false statements, and unfair practices, ensuring borrowers are treated fairly during debt collection.

- Truth in Lending Act (TILA): TILA requires lenders to disclose the terms and costs of borrowing clearly, including interest rates and fees. This transparency helps consumers make informed financial decisions.

Bankruptcy Laws

Bankruptcy offers a legal pathway for individuals and businesses to discharge or restructure debts when repayment becomes impossible. There are different chapters of bankruptcy tailored to specific needs:

- Chapter 7 (Personal): Also known as “liquidation bankruptcy,” it allows individuals to eliminate most unsecured debts by selling non-exempt assets. It’s ideal for those with limited income and substantial debt.

- Chapter 13 (Personal): Known as “reorganization bankruptcy,” this option enables individuals to create a repayment plan over three to five years while keeping their assets. It’s suitable for those with steady incomes who want to catch up on payments like mortgages.

- Chapter 11 (Business): Designed for businesses, Chapter 11 allows companies to restructure debts while continuing operations. It’s often used by larger corporations seeking to recover financially without liquidation.

Statute of Limitations on Debt Collection

The statute of limitations sets a time limit for how long creditors or collectors can sue you to recover unpaid debts. This period varies based on:

- State Laws: Each state has its own rules regarding the statute of limitations, which can range from three to ten years.

- Type of Debt: The timeline depends on whether the debt is related to written contracts, oral agreements, promissory notes, or credit cards.

Once the statute of limitations expires, the debt becomes “time-barred,” meaning collectors can no longer take legal action. However, the debt may still appear on your credit report, and collectors might attempt to negotiate repayment.

How Businesses Handle Outstanding Debt

Managing outstanding debt is a critical aspect of maintaining financial stability for businesses. From internal policies to accounting practices, companies employ a variety of strategies to minimize risks and recover owed funds. These approaches not only ensure smoother cash flow but also protect the business from potential losses due to unpaid debts.

Internal Policies

Businesses establish clear internal policies to manage customer credit and reduce the likelihood of unpaid invoices. These policies include:

- Credit Policies: Companies assess the creditworthiness of customers before extending credit, ensuring that only reliable clients receive favorable terms.

- Payment Terms and Penalties: Clear payment terms are set, such as net-30 or net-60 deadlines, along with penalties for late payments. This encourages timely payments and sets expectations from the outset.

By implementing these measures, businesses can proactively reduce the risk of accumulating bad debts while fostering stronger relationships with creditworthy customers.

Debt Collection Strategies

When customers fail to pay on time, businesses use a range of debt collection strategies to recover owed amounts. These include:

- Reminder Notices: Polite reminders, often sent via email or mail, prompt customers to settle overdue invoices without escalating the situation.

- Collections Agencies: For persistent delinquencies, businesses may hire third-party collections agencies to pursue payments on their behalf. These agencies specialize in debt recovery but may charge a fee or percentage of the collected amount.

- Legal Action: In extreme cases, businesses may take legal action to recover debts, especially if the amount is significant. This step is typically a last resort due to the associated costs and time investment.

Each strategy is tailored to the severity of the situation, balancing the need for recovery with maintaining customer relationships.

Accounting for Bad Debts

Despite best efforts, some debts may become uncollectible, requiring businesses to account for these losses financially. Two common methods are:

Allowance for Doubtful Accounts: Businesses often create a reserve, known as an allowance for doubtful accounts, to anticipate potential bad debts. This proactive approach helps smooth out financial fluctuations caused by uncollected payments.

Write-Offs: When a debt is deemed unrecoverable, it is written off as an expense on the company’s books. This removes the amount from accounts receivable and reflects the loss in financial statements.

Reducing and Avoiding Future Outstanding Debt

Debt can be a useful financial tool when managed wisely, but avoiding excessive or unmanageable debt requires proactive strategies. Both individuals and businesses can adopt practices to reduce existing debt and prevent future financial burdens. By fostering responsible habits and leveraging sound financial planning, it’s possible to maintain control over your financial health.

For Individuals

Individuals can take several steps to minimize debt and avoid falling into financial traps:

- Build an Emergency Fund: Setting aside savings for unexpected expenses, such as medical bills or car repairs, reduces the need to rely on credit cards or loans during emergencies. Aim for three to six months’ worth of living expenses to create a strong safety net.

- Responsible Credit Card Usage: Use credit cards sparingly and pay off balances in full each month to avoid high-interest charges. Keeping credit utilization low also helps maintain a healthy credit score.

- Regularly Monitor Credit Reports: Checking your credit report periodically ensures accuracy and helps you identify potential issues, such as errors or signs of identity theft, before they escalate.

For Businesses

Businesses must adopt disciplined financial management to prevent outstanding debt from hindering growth:

- Strong Credit Management: Establish clear credit policies for customers and assess their creditworthiness before extending terms. This minimizes the risk of late or unpaid invoices.

- Financial Auditing and Forecasting: Regular audits help identify inefficiencies or areas of overspending, while forecasting allows businesses to anticipate cash flow needs and plan for future expenses. These tools ensure better financial decision-making and reduce reliance on borrowing.

General Tips

Certain principles apply universally to both individuals and businesses seeking to manage debt effectively:

- Borrow Strategically: Only take on debt when it adds value, such as purchasing a home, funding education, or investing in business growth. Avoid borrowing for non-essential or depreciating assets.

- Understand Loan Terms Before Borrowing: Carefully review interest rates, repayment schedules, and fees associated with any loan. Fully understanding the terms prevents surprises and ensures affordability.

- Maintain Healthy Credit Practices: Whether personal or corporate, maintaining a strong credit profile is essential. Pay bills on time, keep debts manageable, and avoid maxing out credit limits to build trust with lenders and secure better terms in the future.

By adopting these approaches, individuals and businesses can reduce existing debt, avoid future liabilities, and achieve long-term financial stability. These proactive measures not only protect against financial stress but also pave the way for sustainable growth and success.

Case Studies: Real-World Examples of Outstanding Debt

Examining real-world scenarios provides valuable insights into how outstanding debt can impact households, businesses, and even entire nations. These case studies highlight the challenges faced and the strategies used to recover from financial difficulties, offering lessons for others in similar situations.

Household Facing Medical Debt and Recovery

Consider the story of a middle-class family that accumulated significant medical debt after an unexpected health crisis. With high hospital bills not fully covered by insurance, they turned to credit cards to cover expenses, leading to mounting interest charges. Initially overwhelmed, the family took steps to regain control. Over time, they built an emergency fund to prepare for future unexpected costs. This example underscores the importance of proactive financial planning and the value of negotiating with creditors to ease repayment burdens.

A Startup Mismanaging Vendor Payments

A tech startup experienced rapid growth but struggled with cash flow management due to poor vendor payment practices. The company extended too much credit to clients while delaying payments to suppliers, straining relationships and creating operational bottlenecks. When vendors began demanding immediate payment, the startup faced a liquidity crisis. To recover, the business implemented stricter credit policies for clients, renegotiated payment terms with suppliers, and conducted regular financial audits to monitor cash flow.

Country Facing National Debt Crisis

Greece’s national debt crisis during the early 2010s serves as a stark example of how excessive borrowing can destabilize an entire economy. Years of overspending, tax evasion, and reliance on foreign loans left Greece unable to meet its obligations. The government was forced to implement austerity measures, including deep spending cuts and tax hikes, to secure international bailouts. This case illustrates the broader economic risks of unsustainable national debt, emphasizing the need for responsible fiscal policies and transparent governance to prevent crises.

Conclusion

Understanding and managing outstanding debts is a critical aspect of achieving financial stability, whether for individuals, businesses, or even nations. Throughout this discussion, we’ve explored the various ways debt is recorded, its causes, risks, and the strategies available to reduce or avoid it. From personal contexts like bank statements and credit reports to business liabilities on balance sheets, the importance of accurate documentation and proactive management cannot be overstated.

Key takeaways include the significance of assessing debts systematically, employing effective payment strategies like the snowball or avalanche methods, and leveraging tools like budgeting and negotiation to regain control. For businesses, strong credit policies, regular audits, and strategic borrowing are essential to maintaining liquidity and avoiding cash flow shortages. Additionally, understanding the impact of outstanding debt on credit scores and the broader economy underscores the need for responsible financial practices.

Emphasis on Debt Awareness and Management

Debt awareness is the first step toward empowerment. By regularly monitoring financial health whether through credit reports, balance sheets, or national economic indicators—individuals and organizations can identify potential issues early and take corrective action. Managing debt isn’t just about repaying what’s owed; it’s about creating sustainable habits that prevent future financial strain. This includes building emergency funds, negotiating favorable terms, and making informed borrowing decisions.

Encouragement for Financial Responsibility and Planning

Ultimately, financial responsibility and planning are the cornerstones of long-term success. For households, this means using credit wisely, preparing for unexpected expenses, and staying vigilant about credit utilization. On a macroeconomic level, governments must adopt prudent fiscal policies to ensure sustainable development and avoid crises. By fostering a culture of accountability, transparency, and foresight, we can all work toward a future where debt is a tool for growth, not a source of stress.

In conclusion, while debt is an inevitable part of modern life, how we manage it determines our financial well-being. By staying informed, adopting disciplined strategies, and planning for the future, individuals and organizations alike can navigate the complexities of outstanding debts with confidence and resilience.

FAQs

Can You Get a Mortgage with Outstanding Debt?

Yes, it’s possible to secure a mortgage even with outstanding debts, but approval largely depends on your debt-to-income ratio and overall creditworthiness. Lenders assess your total monthly debt obligations relative to your income to determine your ability to manage mortgage payments. A lower debt-to-income ratio and a strong credit score improve your chances of qualifying. Demonstrating responsible debt management, such as timely payments and low credit utilization, can also work in your favor.

With a Debt Management Plan, What Proportion of the Outstanding Debt Will Be Repaid?

In a debt management plan (DMP), the goal is typically to repay most or all of the outstanding debts, though often with reduced interest rates or waived fees. The exact repayment terms are negotiated with creditors based on individual agreements. These plans consolidate debts into a single monthly payment, making it easier to manage while potentially lowering overall costs. Success depends on adhering to the structured repayment schedule outlined in the DMP.

How to Check for Outstanding Debt

There are several ways to identify and verify outstanding debts:

- Request free annual credit reports from major bureaus like Experian, Equifax, and TransUnion. These reports provide a detailed overview of your debts and payment history.

- Contact lenders, banks, and collections agencies directly to confirm balances and account statuses.

- Use debt management apps or online tools that aggregate financial data to track debts in one place. Regularly monitoring these sources ensures you stay informed about your financial obligations.

How Much Outstanding Debt Was Created by Buying Stocks on Margin?

The amount of outstanding debts created by buying stocks on margin depends on how much was borrowed through a margin account. Margin loans allow investors to borrow funds from brokers to purchase stocks, and these loans are considered outstanding debt until fully repaid. While margin trading can amplify returns, it also increases financial risk, as unpaid balances accrue interest and may require additional collateral if the market moves unfavorably.

What Percentage of Your Credit Score is Based Off of Outstanding Debt?

Outstanding debts accounts for approximately 30% of your credit score, primarily through the credit utilization ratio. This ratio measures the amount of available credit you’re using compared to your total credit limit. Keeping your credit utilization below 30% is recommended to maintain a healthy score. High levels of outstanding debts, especially on revolving accounts like credit cards, can signal financial strain and negatively impact your credit rating.