Fixed Costs: Definition, Examples, and How to Manage Them Effectively

What Are Fixed Costs? A Complete Introduction

Fixed costs represent the foundational, unchanging expenses that both individuals and businesses must pay regularly, irrespective of their income levels, production output, or spending patterns. These costs remain constant over a predetermined period—whether monthly, quarterly, or annually—providing financial predictability in budgeting. Unlike variable costs, which rise and fall with usage (such as electricity bills or grocery expenses), fixed costs stay stable, making them easier to forecast and manage. Examples include rent or mortgage payments, insurance premiums, subscription services, and loan repayments. For businesses, fixed costs might encompass salaries, lease payments, and equipment financing.

Why Understanding Fixed Costs is Crucial for Budgeting

Since fixed costs are consistent, they form the foundation of any financial plan. Knowing these expenses helps individuals and businesses allocate remaining funds toward savings, investments, or discretionary spending.

Common Examples of Fixed Costs in Personal and Business Finance

Personal Fixed Costs

Housing Expenses

These fundamental living costs remain constant regardless of income fluctuations. Housing expenses typically represent the largest fixed cost for most individuals and families, forming the foundation of personal budgets. Whether renting or owning, these payments must be prioritized as they directly impact your living situation. The predictability of housing costs allows for better financial planning, though their inflexibility can create challenges during economic downturns. Understanding these expenses helps in making informed decisions about downsizing, relocating, or refinancing to optimize housing costs.

- Rent or mortgage payments

- Property taxes

- Homeowners’ association (HOA) fees

Insurance Premiums

Insurance costs provide essential financial protection against unexpected life events while remaining predictable in amount and timing. These premiums represent a trade-off between paying for coverage you hope to never use versus being financially devastated by uncovered emergencies. Insurance costs vary by coverage level but remain fixed for policy terms, allowing for accurate budgeting. Regular premium reviews can help identify potential savings through bundling or finding better rates without sacrificing necessary coverage.

- Health insurance

- Car insurance

- Homeowners or renters insurance

Loan Repayments

Fixed loan payments allow borrowers to systematically reduce debt while maintaining budget predictability. These obligations represent contractual agreements with set repayment schedules that don’t fluctuate with income changes. While the fixed nature ensures payment consistency, it also means these costs must be paid even during financial hardship. Understanding loan terms helps borrowers evaluate refinancing opportunities or debt consolidation options to potentially reduce monthly payments.

- Student loans

- Auto loans

- Personal loans

Subscription Services

Modern subscription models provide ongoing access to services and products for predictable recurring fees. These costs have become increasingly prevalent in both personal and professional life, often accumulating unnoticed. While individually small, multiple subscriptions can significantly impact monthly budgets. Regular evaluation helps eliminate unused services and optimize necessary ones through family plans or annual payment discounts.

- Streaming platforms (Netflix, Spotify)

- Gym memberships

- Software subscriptions (Microsoft 365, Adobe Creative Cloud)

Other Recurring Expenses

These essential modern living costs maintain consistent payment amounts and schedules. While sometimes overlooked, they form the infrastructure supporting daily life and work. Their fixed nature facilitates budgeting but requires periodic review to ensure you’re getting optimal value. Many of these services offer opportunities for savings through negotiation, promotional rates, or alternative providers.

- Cell phone plans

- Internet services

- Childcare or tuition fees

Business Fixed Costs

These unchanging operational expenses form the foundation of a company’s financial structure. They must be paid regardless of sales volume or production output, creating a baseline for break-even analysis. While inflexible in the short term, strategic management of these costs can significantly impact profitability and cash flow stability.

Operational Expenses

The fundamental costs required to keep business facilities and staff functioning. These expenses remain relatively constant across normal production ranges, providing stability in financial planning but also creating financial pressure during slow periods.

- Office or warehouse rent

- Equipment leases

- Salaries of full-time employees

Insurance & Legal Fees

Essential business protections that mitigate operational risks through predictable payment structures. These costs safeguard against catastrophic financial losses while maintaining compliance with legal requirements. Premiums and fees are typically negotiable at renewal periods.

- Business liability insurance

- Licensing and permit fees

Technology & Software Costs

Digital infrastructure expenses that maintain business operations and competitiveness. These fixed costs have become increasingly important in modern business environments, often replacing more variable traditional expenses. Many offer scalable options to align with business growth.

- Annual software licenses

- Cloud storage subscriptions

Fixed Costs vs. Variable Costs: A Detailed Comparison

| Aspect | Fixed Costs | Variable Costs |

|---|---|---|

| Definition | Remain constant | Change based on usage |

| Examples | Rent, insurance, subscriptions | Groceries, utilities, fuel |

| Predictability | Easy to forecast | Fluctuates monthly |

| Flexibility | Harder to adjust quickly | Can be reduced more easily |

Why Both Matter in Financial Planning ?

A balanced financial plan requires managing both fixed and variable costs effectively. Here’s why each plays a critical role:

Fixed Costs Provide Stability

Fixed costs like rent, insurance, and loan payments remain constant, creating a predictable foundation for your budget. This stability helps individuals and businesses:

- Plan long-term financial commitments with confidence

- Maintain essential operations even during slow periods

- Calculate minimum income requirements for sustainability

Variable Costs Offer Flexibility

Expenses like groceries, utilities, and fuel fluctuate based on usage, providing important spending flexibility. This variability allows for:

- Immediate cost-cutting when financial adjustments are needed

- Scaling expenses up or down based on income changes

- Better cash flow management during economic fluctuations

The Strategic Balance

The interplay between fixed and variable costs creates a healthy financial ecosystem:

- Fixed costs establish your baseline financial obligations

- Variable costs provide adjustable spending capacity

- Together they enable both stability and adaptability in your finances

Smart financial management involves:

- Keeping fixed costs at sustainable levels

- Maintaining awareness of variable cost patterns

- Creating buffer room between the two for financial resilience

This dual approach ensures you can meet essential obligations while retaining the flexibility to adapt to changing circumstances.

How Fixed Costs Impact Your Budget

Advantages of Fixed Costs

- Predictability – Consistent amounts make budgeting and forecasting easier.

- Stability – Provides financial security since payments don’t fluctuate.

- Easier Cash Flow Management – Businesses and individuals can plan around known expenses.

- Lower Financial Stress – No surprises in essential payments.

- Better Loan Approvals – Lenders prefer stable, predictable expenses when assessing creditworthiness.

- Simplified Financial Planning – Helps set clear savings and investment goals.

- Scalability Benefits (For Businesses) – Higher production doesn’t increase fixed costs, improving profit margins at scale.

- Predictability – Easier to plan long-term budgets.

- Stability – Helps avoid sudden financial shocks.

Disadvantages of Fixed Costs

- Lack of Flexibility – Hard to reduce quickly in financial emergencies.

- High Fixed Costs = Less Disposable Income – Leaves less room for savings or discretionary spending.

- Financial Strain During Downturns – Must be paid even if income drops (job loss, business slowdown).

- Long-Term Commitments – Contracts (leases, loans) lock you into payments, limiting adaptability.

- Opportunity Cost – Money tied up in fixed expenses could be invested elsewhere.

- Risk of Overhead Burden (For Businesses) – High fixed costs can hurt profitability in slow seasons.

- Inflation Vulnerability – Fixed payments lose value over time if income doesn’t keep up with rising costs.

How Fixed Costs Affect Saving & Spending Habits

- If fixed costs consume too much income, less is left for savings.

- Balancing fixed and variable costs is key to financial health.

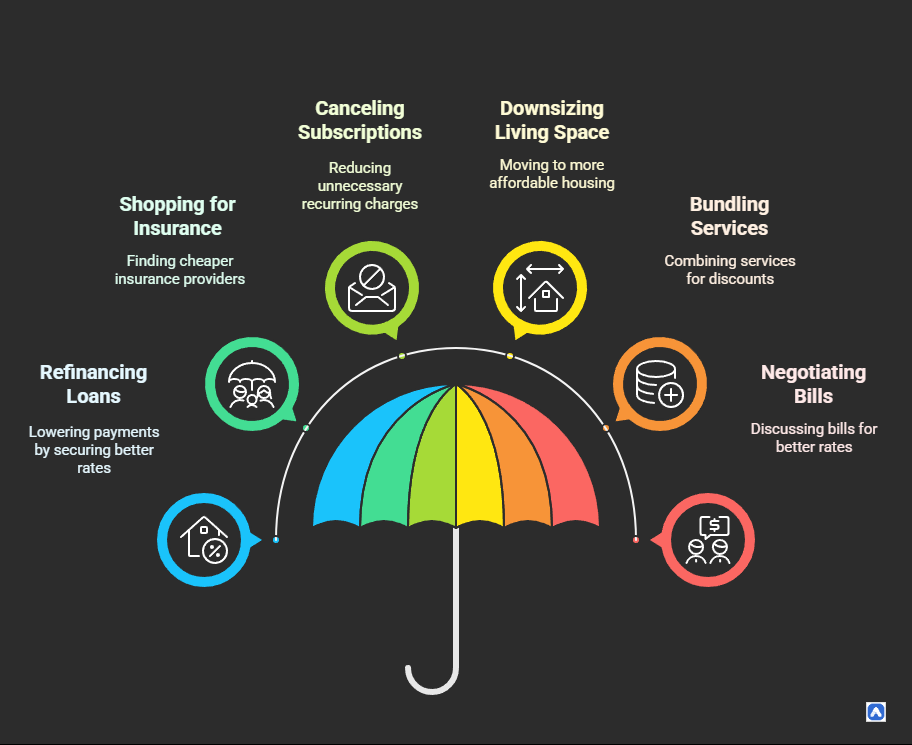

How to Manage and Reduce Fixed Costs

1. Refinance Loans or Mortgages

Refinancing existing debt can significantly lower your monthly payments by securing a better interest rate. This is particularly effective when market rates drop or your credit score improves. Consider refinancing:

- Mortgages (potentially saving thousands over the loan term)

- Auto loans (shorter terms may offer bigger savings)

- Student loans (federal and private loan refinancing options)

Tip: Calculate break-even points (fees vs. savings) before refinancing.

2. Shop Around for Cheaper Insurance

Annual policy reviews can uncover substantial savings across all insurance types:

- Compare at least 3-5 providers annually

- Ask about bundling discounts (home+auto policies)

- Increase deductibles for lower premiums

- Inquire about loyalty or claim-free discounts

Best time to shop: 30-45 days before policy renewal.

3. Cancel or Downgrade Unused Subscriptions

The “subscription economy” often leads to unnoticed recurring charges. Conduct a 3-step audit:

- List all active subscriptions (check bank statements)

- Identify unused or redundant services

- Downgrade premium plans to basic tiers

Potential savings: 50−50−200/month for average households.

4. Downsize Your Living Space

Housing is typically the largest fixed cost. Downsizing options include:

- Moving to a smaller apartment/home

- Getting roommates to split costs

- Negotiating rent with landlords

- Relocating to more affordable areas

Consider: Weigh moving costs against long-term savings.

5. Bundle Services for Discounts

Service providers often offer package deals:

- Internet + TV + phone bundles

- Insurance multi-policy discounts

- Family plans for streaming services

Warning: Avoid paying for unneeded services just for bundles.

6. Negotiate with Service Providers

Many recurring bills have negotiation flexibility:

- Cable/internet providers (ask for retention deals)

- Cell phone carriers (loyalty discounts)

- Gym memberships (off-peak rates)

- Credit card annual fees

Pro tip: Ask “What promotions are available?” rather than demanding discounts.

Bonus Strategy: Automate Payments

Many providers offer 2-5% discounts for:

- Auto-pay enrollment

- Paperless billing

- Annual vs. monthly payment plans

Each strategy requires some initial effort but can lead to significant long-term savings. The key is periodic review – set calendar reminders to reassess these costs quarterly or annually. Even small reductions in multiple fixed costs can collectively free up hundreds in your monthly budget.

Fixed Costs in Business vs. Personal Finance

In business, fixed costs like rent, salaries, and equipment leases create a financial baseline that doesn’t fluctuate with sales. These expenses provide stability but can strain cash flow during slow periods, directly impacting profitability. Companies must carefully manage these costs to maintain healthy margins, often through renegotiating leases, outsourcing, or switching to scalable solutions like cloud services instead of physical infrastructure.

For individuals, fixed costs such as mortgage payments, car loans, and insurance premiums form the foundation of household budgets. Unlike businesses, personal fixed costs offer less flexibility and must be paid regardless of income changes, making them riskier during job loss or financial hardship. Effective management involves refinancing high-interest debts, downsizing living arrangements, and eliminating unnecessary subscriptions to maintain financial security. Both scenarios highlight how fixed costs, while predictable, require proactive strategies to prevent them from becoming financial burdens.s.

Key Differences Between Business & Personal Fixed Costs

| Factor | Business Fixed Costs | Personal Fixed Costs |

|---|---|---|

| Flexibility | Can renegotiate leases, outsource | Harder to adjust quickly |

| Impact of Loss | Affects profitability & sustainability | Risks credit score & financial stability |

| Tax Benefits | Often tax-deductible | Limited deductions (e.g., mortgage interest) |

Best Tools to Track Fixed Costs

| Category | Tool/Feature | Description |

|---|---|---|

| Budgeting Apps | Mint | Automatically categorizes expenses. |

| YNAB (You Need A Budget) | Helps allocate funds efficiently. | |

| Spreadsheet Templates | Google Sheets or Excel | Manual tracking of expenses and budgets. |

| Bank Features | Auto-categorization | Automatically categorizes recurring payments. |

Financial Advice by Life Stage

Young Adults (18-30)

Focus: Managing rent & student loans.

- Rent is often the biggest expense—always pay it first to avoid late fees.

- Break student loan payments into smaller, automatic transfers to stay on track.

- Use budgeting apps (like Mint) to track spending and avoid overspending on non-essentials (e.g., eating out, subscriptions).

Married Couples (30-50)

Focus: Joint budgeting for household costs.

- Combine incomes but set clear spending limits to avoid conflicts.

- Automate bills (mortgage, utilities, insurance) so nothing gets missed.

- Save for emergencies (3-6 months’ expenses) and future goals (kids’ education, vacations).

Seniors (60+)

Focus: Fixed income management (healthcare & housing).

- Pay Medicare/insurance premiums first—health costs are a top priority.

- Consider downsizing or refinancing housing to free up cash.

- Take advantage of senior discounts (groceries, prescriptions, public transport) to stretch your budget.

Expert Tips to Balance Fixed and Variable Expenses

1. Apply the 50/30/20 Budgeting Rule

Split your income into 50% for needs (rent, groceries, bills), 30% for wants (dining out, entertainment), and 20% for savings or debt payoff. This ensures balanced spending while securing your future.

2. Build an Emergency Fund

Save 3–6 months’ worth of essential expenses (rent, utilities, food) in a separate account to cover unexpected crises (job loss, medical bills) without going into debt.

3. Automate Payments

Set up auto-pay for bills and savings to avoid late fees, boost credit scores, and ensure consistent savings without forgetting.

Final Thoughts: Optimizing Fixed Costs for Financial Stability

Fixed costs—like rent, loan payments, and insurance—are essential expenses that stay the same each month. While you can’t eliminate them, managing them wisely ensures financial stability. Start by reviewing these costs periodically to identify areas for savings, such as refinancing loans or negotiating bills. Cutting even small amounts from fixed expenses frees up cash for savings or emergencies. The key is to strike a balance between fixed and variable costs, so your budget remains flexible enough to handle unexpected changes without stress.

By optimizing fixed expenses, you gain greater control over your finances. This not only prevents overspending but also creates room for future goals, like investing or paying off debt. Over time, smart management of fixed costs builds a stronger financial foundation, reducing anxiety and helping you achieve long-term security. A disciplined approach—tracking, adjusting, and prioritizing—turns unavoidable expenses into a tool for stability rather than a burden.

Key Takeaways:

- Review fixed costs periodically.

- Reduce where possible (refinance, negotiate).

- Balance with variable expenses for flexibility.

By optimizing fixed costs, you gain better control over your budget—leading to long-term financial security.

FAQS

What exactly are fixed costs in business?

A: Fixed costs in business are expenses like rent, salaries, and equipment leases that stay constant regardless of sales volume. These differ from variable costs (like raw materials) that fluctuate with production.

How do fixed costs differ from variable costs?

A: The main difference between fixed and variable costs is predictability – fixed costs (mortgage, insurance) remain stable, while variable costs (groceries, utilities) change monthly based on usage.

Why is understanding fixed costs important for budgeting?

A: Knowing your fixed costs helps create a stable budget foundation since these predictable expenses (like loan payments or subscriptions) must be paid first before allocating other funds.

What are common examples of fixed costs in personal finance?

A: Typical personal fixed costs include mortgage/rent payments, car loans, insurance premiums, and subscription services – expenses that remain constant month-to-month.

How can I calculate my total fixed costs?

A: To calculate fixed costs, list all expenses with consistent amounts (rent, loans, memberships) and sum them. Business fixed costs include additional items like equipment leases and salaries.

What happens if my fixed costs are too high?

A: Excessive fixed costs reduce financial flexibility. Solutions include refinancing loans, downsizing living space, or canceling unused subscriptions to lower these mandatory expenses.

How do fixed costs impact business profitability?

A: High fixed costs require greater sales volume to break even, but once covered, each additional sale contributes more directly to profits (called operating leverage).

Can fixed costs ever become variable?

A: Some fixed costs can become semi-variable (like salaries with commission components). Businesses may convert fixed costs (office space) to variable (co-working memberships) for flexibility.