Financial Literacy for Life: How to Make Smarter Money Moves

Introduction to Financial Literacy

Financial literacy is the foundation of a stable and prosperous life. It refers to the ability to understand and effectively use various financial skills, including personal financial management, budgeting, investing, and debt management.

Without financial literacy, individuals may struggle with debt, poor savings habits, and inadequate retirement planning.

Core Components of Financial Literacy

Financial literacy encompasses several key areas:

- Budgeting: Managing income and expenses to live within your means.

- Saving: Setting aside money for emergencies, goals, and future needs.

- Investing: Growing wealth through stocks, bonds, real estate, and other assets.

- Credit and Debt Management: Understanding how credit works and managing loans responsibly.

- Retirement Planning: Preparing for financial independence in later years.

- Insurance and Risk Management: Protecting against financial losses due to unforeseen events.

- Tax Understanding: Knowing how taxes impact income and investments.

By mastering these areas, individuals can make informed financial decisions, avoid common pitfalls, and build long-term wealth.

Why Financial Literacy is Important

Financial literacy is the essential knowledge and skill set required to manage money wisely. This ensures long-term financial stability and growth. It involves understanding budgeting, saving, investing, debt management, and retirement planning to make informed financial decisions. A strong grasp of financial literacy helps individuals avoid debt traps, build emergency funds, and secure their future through smart investments.

Personal Benefits

Financial literacy empowers individuals to take control of their finances. With a strong understanding of money management, people can:

- Make better financial decisions by evaluating options like loans, investments, and insurance policies.

- Avoid debt traps by understanding interest rates and responsible borrowing.

- Develop strong savings habits, ensuring financial security during emergencies.

- Achieve financial independence by making informed choices about spending, saving, and investing.

National and Societal Benefits

A financially literate population contributes to economic stability. When people manage money wisely, it reduces poverty and inequality by helping individuals escape cycles of debt. It promotes economic growth as people invest and spend responsibly.

- Reduces poverty and inequality by helping individuals escape cycles of debt.

- Promotes economic growth as people invest and spend responsibly.

- Encourages responsible borrowing and lending, reducing financial crises.

- Creates better-informed citizens who can advocate for fair financial policies.

Common Consequences of Low Financial Literacy

Those lacking financial education often face:

- High-interest debt from credit cards or predatory loans.

- Poor credit scores, making it harder to secure mortgages or loans.

- Inadequate retirement savings, leading to financial stress in old age.

- Higher susceptibility to scams due to a lack of awareness about financial fraud.

When is Financial Literacy Month?

April is recognized as Financial Literacy Month in the United States and many other countries around the world.

This annual observance serves as a dedicated time to highlight the importance of financial education and empower individuals to take control of their financial futures.

1. Workshops and Webinars Hosted by Financial Experts

- Interactive Learning: Financial experts, advisors, and educators conduct workshops and webinars on topics like budgeting, saving, investing, debt management, and retirement planning.

- Accessibility: Many of these events are free and open to the public, often held both in-person and online to reach a wider audience.

- Real-World Insights: Participants gain practical advice and actionable tips tailored to various life stages and financial situations.

For example:

- A local bank might host a seminar on “How to Build Credit Responsibly.”

- A nonprofit organization could offer a webinar on “Saving for College: 529 Plans Explained.”

2. School Programs Teaching Kids About Saving and Budgeting

- Early Education: Schools integrate financial literacy into their curricula during April, teaching students foundational concepts such as saving, budgeting, and understanding the value of money.

- Hands-On Activities: Teachers use engaging methods like games, simulations, and real-life scenarios to make learning fun and relatable.

- Long-Term Impact: Educating children early helps instill healthy financial habits that will benefit them throughout their lives.

Examples include:

- Classroom exercises where students create mock budgets or run a pretend business.

- Guest speakers from banks or credit unions explaining how savings accounts work.

3. Public Campaigns Encouraging Responsible Money Habits

- Awareness Drives: Governments and nonprofits launch nationwide campaigns to spread the message of financial responsibility. These campaigns often focus on key themes like avoiding debt traps, building emergency funds, and planning for retirement.

- Social Media Outreach: Platforms like Facebook, Instagram, and Twitter are used to share infographics, videos, and tips that resonate with younger audiences.

- Community Events: Local libraries, community centers, and businesses may host events such as free tax preparation assistance or “Money Smart” workshops.

For instance:

- A campaign slogan like “Save Today, Secure Tomorrow” encourages people to prioritize saving over impulse spending.

- Infographics shared online explain the power of compound interest or the dangers of high-interest payday loans.

4. Promotion of Resources by Financial Institutions

- Free Tools and Guides: Banks, credit unions, and investment firms release educational materials, apps, and tools to help individuals manage their finances better. Examples include budget templates, savings calculators, and credit score trackers.

- Incentive Programs: Some institutions offer promotions during April, such as waived fees for opening a savings account or discounts on financial planning services.

- Personalized Support: Customers can access one-on-one consultations with financial advisors to discuss their unique goals and challenges.

5. Collaboration Between Nonprofits and Governments

- Partnerships: Nonprofit organizations often collaborate with government agencies to amplify their impact. For example, the U.S. Department of the Treasury partners with groups like the National Endowment for Financial Education (NEFE) to distribute free resources.

- Policy Advocacy: Governments may use Financial Literacy Month to advocate for policies that promote financial education in schools and workplaces.

- Grants and Funding: Additional funding may be allocated to support financial literacy programs targeting underserved communities.

Financial institutions, nonprofits, and governments use this month to promote resources that help people improve their financial knowledge.

Who Benefits from Financial Literacy Month?

Everyone can benefit from the resources and initiatives offered during Financial Literacy Month, regardless of age, income level, or financial experience. Specific groups that particularly benefit include:

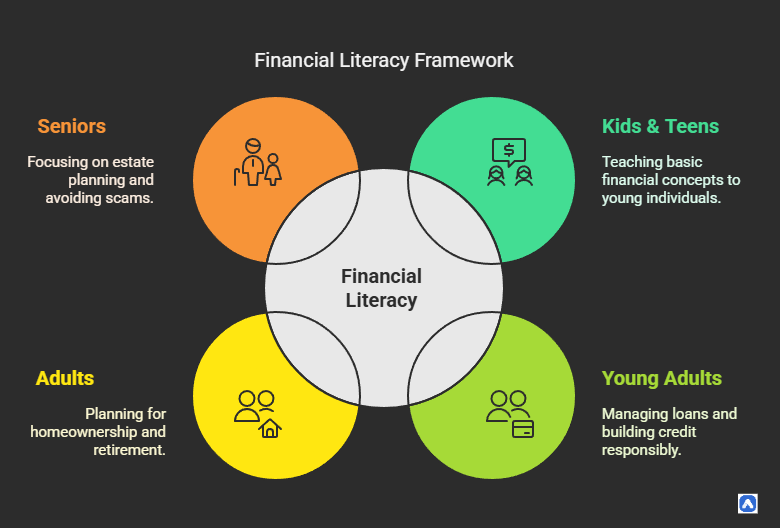

- Young Adults: Learning how to manage student loans, build credit, and start saving early.

- Families: Gaining tools to teach kids about money and plan for future expenses like college tuition.

- Seniors: Understanding how to protect their assets, avoid scams, and navigate retirement.

- Underserved Communities: Accessing free or low-cost financial education to break cycles of poverty.

Why April Matters ?

Designating April as Financial Literacy Month creates a unified effort to address the widespread lack of financial knowledge. It provides an opportunity for individuals to pause, reflect on their financial habits, and commit to improving them.Moreover, it fosters a culture of accountability and empowerment, reminding us that financial health is within everyone’s reach with the right tools and mindset.t provides an opportunity for individuals to pause, reflect on their financial habits, and commit to improving them.

Moreover, it fosters a culture of accountability and empowerment, reminding us that financial health is within everyone’s reach with the right tools and mindset. By participating in Financial Literacy Month activities, you not only enhance your own financial literacy but also contribute to creating a more financially savvy society—one person at a time.

How to Learn Financial Literacy

1. Self-Education

Books like Rich Dad Poor Dad by Robert Kiyosaki and The Total Money Makeover by Dave Ramsey provide foundational knowledge. Podcasts (Planet Money, The Dave Ramsey Show) and YouTube channels (Graham Stephan, The Financial Diet) offer free, accessible advice.

2. Online Courses & Platforms

Free courses on Khan Academy, Coursera, and edX cover budgeting, investing, and debt management. Paid platforms like Udemy and MasterClass offer in-depth lessons from financial experts.

3. Apps and Tools

- Budgeting: Mint and YNAB (You Need A Budget) help track spending.

- Investing: Robinhood, Acorns, and Stash simplify stock market participation.

- Credit Tracking: Credit Karma monitors credit scores for free.

4. Financial Advisors & Coaches

Certified Financial Planners (CFPs) provide personalized advice. Nonprofit organizations like the National Foundation for Credit Counseling (NFCC) offer free or low-cost counseling.

5. School and Workplace Programs

Many schools now integrate financial literacy into curricula. Employers may offer financial wellness programs, including retirement planning workshops.

Key Areas of Financial Literacy

1. Budgeting & Money Management

A budget is the foundation of financial literacy, helping individuals track income and expenses to ensure spending aligns with their financial goals. By categorizing expenses into needs, wants, and savings, tools like the 50/30/20 rule simplify money management: 50% for essential needs (housing, food), 30% for discretionary wants (entertainment), and 20% for savings or debt repayment. Budgeting fosters discipline, prevents overspending, and identifies areas for improvement. It also allows individuals to allocate funds for short-term goals (vacations) and long-term objectives (homeownership). Regularly reviewing and adjusting your budget ensures it remains realistic and effective in achieving financial stability.

Saving is a critical habit that provides financial security and peace of mind. An emergency fund , typically covering 3–6 months of living expenses, acts as a safety net during unexpected events like job loss or medical emergencies. This fund should be kept in a high-yield savings account to maximize interest earnings while ensuring liquidity. Building an emergency fund starts small—saving even $50 a month adds up over time. Prioritizing savings not only protects against debt but also empowers individuals to achieve future goals like buying a home or starting a business. Consistent saving is key to long-term financial resilience.

3. Understanding Credit

Credit plays a pivotal role in financial health, influencing loan approvals, interest rates, and even rental applications. Credit scores, measured by systems like FICO or VantageScore , range from 300 to 850 and reflect creditworthiness. Responsible credit card use—paying bills on time, keeping balances low, and avoiding unnecessary debt—builds a strong credit history. A good score unlocks lower interest rates on mortgages and car loans, saving thousands over time. Conversely, poor credit limits opportunities and increases borrowing costs. Understanding how credit works helps individuals make informed decisions and maintain financial credibility.

4. Debt Management

Debt can either build wealth or create financial strain, depending on its type and management. Good debt , such as mortgages or student loans, often leads to asset growth or increased earning potential. In contrast, bad debt , like high-interest credit cards, drains finances without offering long-term benefits. Strategies like the debt avalanche method (paying off debts with the highest interest first) save money on interest, while the snowball method (paying smallest debts first) builds momentum through quick wins. Consolidating debts or negotiating lower interest rates can also ease repayment. Managing debt responsibly ensures financial freedom and prevents overwhelming obligations.

5. Investing Basics

Investing is a powerful way to grow wealth over time by putting money into assets like stocks, bonds, mutual funds, or ETFs. Stocks offer higher returns but come with greater risk, while bonds provide stability and predictable income. Mutual funds and ETFs allow diversification, spreading risk across multiple investments. Retirement accounts like 401(k)s and IRAs offer tax advantages, making them ideal for long-term savings. Understanding risk tolerance and investment goals is crucial before diving in. Compound interest amplifies returns when investing early, turning modest contributions into significant wealth over decades. Educating yourself on investing basics lays the groundwork for financial independence.

6. Insurance & Risk Protection

Insurance is a vital tool for managing financial risks and protecting against unforeseen events. Policies like health insurance , auto insurance , homeowners insurance , and life insurance safeguard against costly emergencies. For instance, health insurance reduces medical expenses, while life insurance ensures loved ones are financially secure after a breadwinner’s passing. Adequate coverage prevents out-of-pocket expenses that could derail financial stability. Evaluating policies regularly ensures they meet current needs and lifestyle changes. While premiums may seem like an added expense, insurance ultimately provides peace of mind and shields individuals from catastrophic financial losses.

7. Tax Knowledge

Understanding taxes is essential for maximizing income and minimizing liabilities. Tax brackets determine how much you owe based on earnings, while deductions and credits reduce taxable income. Contributions to retirement accounts like IRAs or 401(k)s often qualify for tax breaks, lowering overall liability. Filing taxes accurately ensures compliance and avoids penalties, while strategic planning maximizes refunds. Staying informed about tax laws helps individuals take advantage of incentives like education credits or energy-efficient home improvements. Basic tax knowledge empowers individuals to navigate filings confidently and retain more of their hard-earned money.

8. Retirement Planning

Retirement planning ensures financial security during later years when regular income ceases. Starting early leverages compound interest , allowing small contributions to grow significantly over decades. Employer-sponsored plans like 401(k)s often include matching contributions, essentially free money. Individual accounts like Roth IRAs provide flexibility and tax-free withdrawals in retirement. Setting clear goals—such as desired retirement age or lifestyle—guides contribution amounts and investment choices. Without proper planning, retirees risk outliving their savings or facing reduced quality of life. Proactive retirement planning guarantees comfort and independence in your golden years.

Teaching Financial Literacy at Different Life Stages

Financial literacy isn’t a one-size-fits-all concept—it evolves as individuals progress through different stages of life. Tailoring financial education to each stage ensures that people develop the skills and habits needed to navigate their unique financial challenges and opportunities. Here’s how financial literacy can be taught across various life stages:

Common Myths and Misconceptions

By participating in Financial Literacy Month activities, you not only enhance your own financial literacy but also contribute to creating a more financially savvy society—one person at a time.

- “You need to be rich to invest.” → Even small, consistent investments grow over time.

- “Credit cards are always bad.” → Used wisely, they build credit and offer rewards.

- “I don’t need to think about retirement yet.” → Starting early maximizes compound growth.

Financial Literacy in the Digital Age

The rapid evolution of technology has transformed the way we manage money, introducing new tools and platforms that offer convenience but also require a heightened level of financial awareness. In today’s digital age, financial literacy must expand to include understanding emerging trends like cryptocurrencies , digital wallets , Buy Now, Pay Later (BNPL) services , and the importance of online banking security .

1. Cryptocurrencies and Digital Wallets

Cryptocurrencies like Bitcoin and Ethereum have gained popularity as alternative forms of currency and investment. While they offer opportunities for growth and decentralized transactions, they also come with risks, including high volatility and lack of regulation. Understanding how blockchain technology works and the mechanics of buying, selling, and storing cryptocurrencies is essential for anyone considering entering this space.

Digital wallets, which store cryptocurrencies and enable contactless payments, are another key innovation. However, users must grasp the importance of securing private keys and protecting their accounts from hacking or phishing attacks. Without proper knowledge, individuals risk losing their assets or falling victim to scams.

2. Buy Now, Pay Later (BNPL) Services

BNPL platforms like Klarna, Afterpay, and Affirm allow consumers to make purchases and pay them off in installments, often without interest. While these services can provide flexibility, they may also encourage overspending or lead to debt if not managed responsibly. Financial literacy in this area involves understanding terms and conditions, recognizing hidden fees, and avoiding over-reliance on short-term credit solutions.

3. Online Banking and Fraud Prevention

Online banking has revolutionized the way we handle finances, offering 24/7 access to accounts, bill payments, and money transfers. However, it also exposes users to cyber threats such as identity theft, phishing scams, and unauthorized transactions. To stay safe, individuals need to adopt best practices like using strong passwords, enabling two-factor authentication, monitoring account activity regularly, and being cautious about sharing personal information online.

Financial Goals and Planning

Setting clear financial goals is a cornerstone of effective money management. Without a roadmap, it’s easy to lose sight of your priorities and fall into financial disarray. The key to successful goal-setting lies in creating SMART goals —Specific, Measurable, Achievable, Relevant, and Time-bound. This framework ensures your objectives are well-defined and attainable, providing a clear path toward financial success. Once your goals are set, regularly tracking progress and making adjustments as needed will keep you on course, even when life throws unexpected challenges your way.

The SMART Framework for Financial Goals

- Specific: Clearly define what you want to achieve. For example, instead of saying “I want to save more,” specify “I want to save $10,000 for a down payment on a house.”

- Measurable: Ensure your goal can be quantified so you can track progress. For instance, “Save $500 per month” is measurable, while “Save more money” is not.

- Achievable: Set realistic goals based on your income, expenses, and current financial situation. Saving $1 million in a year on a modest salary may not be feasible, but saving $5,000 might be.

- Relevant: Align your goals with your broader life objectives. For example, paying off student loans may take priority over investing if high-interest debt is holding you back.

- Time-bound: Assign a deadline to create urgency and focus. Instead of saying “I’ll start saving for retirement someday,” commit to “I’ll contribute $200/month to my IRA starting this year.”

Measuring Financial Literacy

Measuring financial literacy is essential to understanding your strengths and identifying areas for improvement. Tools like quizzes and assessments, such as those found in the National Financial Capability Study , provide a structured way to evaluate key competencies, including budgeting, saving, investing, and debt management. These quizzes often cover practical scenarios, helping individuals gauge their ability to make informed financial decisions.

Regular self-checks foster continuous learning and growth, allowing you to track progress over time. For example, retaking a financial literacy quiz every six months can highlight improvements or reveal gaps in knowledge. Beyond formal assessments, reflecting on personal financial habits such as sticking to a budget or avoiding high-interest debt also serves as a valuable measure of literacy. By consistently measuring and refining your financial skills, you can build confidence and achieve greater financial well-being.

Conclusion: Unlock Your Path to Financial Freedom

Financial literacy isn’t just about numbers—it’s about freedom, security, and peace of mind. By mastering budgeting, smart investing, and debt management, you take control of your future instead of leaving it to chance. Every small step—tracking expenses, building an emergency fund, or learning how compound interest works—adds up to lasting wealth and independence.

Imagine a life free from money stress, where you confidently make decisions that grow your savings, protect your family, and secure your retirement. That life is within your reach—starting today. Whether you’re just beginning or refining your strategy, financial literacy is the key to unlocking opportunities and avoiding costly mistakes.

Don’t wait for “someday.” Your future self will thank you for the knowledge you gain now. Take action—read, learn, and apply these principles. Financial freedom isn’t a dream; it’s a choice. Make it yours.