Is a Debt Management Plan Right for You? (The Truth Revealed)

Debt can feel overwhelming, but with the right debt management strategies, you can take control of your finances and work toward a debt-free future. Whether you’re struggling with credit card debt, personal loans, or medical bills, understanding how to manage and repay debt effectively is crucial for long-term financial stability.

In this guide, we’ll cover:

- What debt management is and why it matters

- Different types of debt and how they impact your finances

- Proven debt repayment strategies like the Debt Snowball and Debt Avalanche methods

- How debt management plans (DMPs) and credit counseling can help

- The role of debt management companies and how to choose the best debt management programs

- Tips for avoiding debt traps and maintaining financial discipline

By the end, you’ll have a clear roadmap to tackle your debt and achieve financial freedom.

Introduction to Debt Management

What is Debt Management?

Debt management refers to the process of organizing, repaying, and reducing debt in a structured way. It involves creating a realistic repayment plan, negotiating with creditors, and sometimes enrolling in a debt management plan (DMP) through a credit counseling agency. Debt management is a structured approach to handling and repaying debts efficiently, ensuring that individuals maintain control over their financial obligations without compromising their long-term fiscal health. At its core, debt management involves creating a strategic plan to address outstanding debts, prioritize repayments, and negotiate better terms with creditors. This process not only alleviates the stress associated with mounting financial burdens but also lays the foundation for sustainable financial stability.

Why Managing Debt is Essential for Financial Well-Being

The importance of managing debt cannot be overstated, especially in today’s consumer-driven economy where access to credit is readily available. Poorly managed debt can severely affect an individual’s creditworthiness, making it difficult to secure loans, mortgages, or even rental agreements. Moreover, excessive debt often leads to emotional stress, impacting mental health and overall quality of life. By adopting best debt management programs , individuals can break free from the cycle of debt and focus on building wealth and achieving their financial goals.

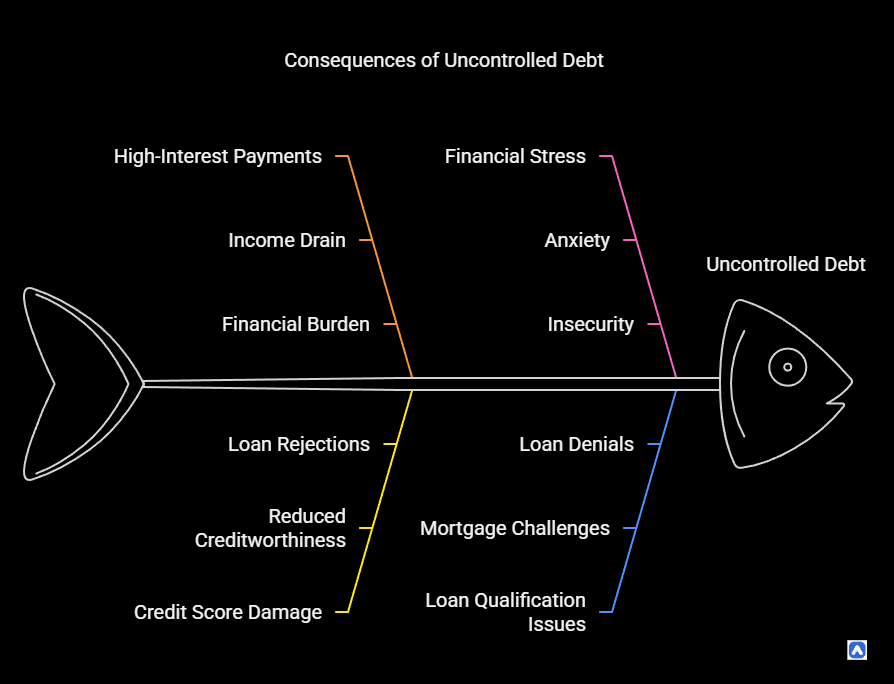

Uncontrolled debt can lead to:

- High-interest payments that drain your income

- Damage to your credit score

- Stress and financial insecurity

- Difficulty qualifying for loans or mortgages

A solid debt management strategy helps you:

- Lower interest rates and monthly payments

- Avoid bankruptcy or default

- Improve your credit score over time

Common Reasons People Fall Into Debt

Common reasons why people fall into debt include overspending, medical emergencies, unemployment, or unexpected life events. While these situations are often beyond one’s control, proactive debt management strategies can mitigate their impact. Whether through budgeting tools, credit counseling, or working with reputable debt management companies , there are numerous resources available to guide individuals toward financial recovery. Ultimately, understanding how does debt management work empowers individuals to take charge of their finances, avoid common pitfalls, and pave the way for a debt-free future.

- Medical emergencies (unexpected bills)

- Job loss or reduced income

- Overspending with credit cards

- Lack of an emergency fund

- Predatory lending (payday loans, high-interest financing)

Understanding Different Types of Debt

Debt comes in various forms, each with distinct characteristics that influence how they should be managed. Broadly, debt can be categorized into two main types: secured and unsecured . Secured debt is backed by collateral, such as a house in the case of a mortgage or a car for an auto loan. If the borrower defaults, the lender has the right to seize the asset used as security. This type of debt typically carries lower interest rates due to the reduced risk for lenders. In contrast, unsecured debt , like credit cards and personal loans, does not require collateral. Because of the higher risk involved, unsecured debts usually come with higher interest rates. Not all debt is created equal. Knowing the differences can help you prioritize repayments.

Secured vs. Unsecured Debt

- Secured debt is backed by collateral (e.g., mortgages, auto loans). Failure to pay can lead to repossession.

- Unsecured debt (e.g., credit cards, medical bills) has no collateral but may result in collections or lawsuits.

Revolving Credit vs. Installment Loans

- Revolving credit (credit cards, lines of credit) has variable payments and high interest.

- Installment loans (mortgages, student loans) have fixed payments over time.

Good Debt vs. Bad Debt

| Aspect | Good Debt (Smart Debt Management) | Bad Debt (Poor Debt Management) |

|---|---|---|

| Debt Management Strategy | Helps build wealth and financial stability. Proper planning ensures manageable repayment. | Leads to financial strain due to high-interest rates and impulsive borrowing. |

| Purpose | Used for investments that appreciate in value (e.g., homeownership, education). | Used for short-term wants, often with no lasting financial benefit. |

| Examples | Mortgages, student loans, business loans. | High-interest credit cards, payday loans, personal loans for luxuries. |

| Impact on Net Worth | Can increase net worth over time when managed properly. | Can reduce financial security and create long-term debt cycles. |

| Interest Rates | Lower interest rates, making repayment more manageable. | High-interest rates that make it difficult to pay off debt quickly. |

| Repayment Terms | Typically long-term, with structured payments that align with income. | Short-term loans with high monthly payments, leading to financial burden. |

| Risk | Lower risk when managed wisely, often tied to appreciating assets. | High risk of financial distress if payments are missed or debt accumulates. |

- Good debt can increase net worth (e.g., mortgages, student loans).

- Bad debt (high-interest credit cards, payday loans) drains finances without long-term benefits.

Evaluating Your Debt Situation

To effectively manage your financial health, the first step is gaining a clear understanding of your current debt situation. Start by calculating your total debt , which includes all outstanding balances across credit cards, loans, and other financial obligations. Add up the principal amounts owed, along with any accrued interest, to determine the full scope of what you owe. This figure provides a baseline for assessing your financial standing and serves as a starting point for creating a debt management plan .

How to Calculate Your Total Debt

List all debts, including:

- Credit cards

- Personal loans

- Medical bills

- Auto loans

- Student loans

Understanding Debt-to-Income (DTI) Ratio

Your DTI ratio compares monthly debt payments to gross income. Lenders prefer a DTI below 36%.

Formula:

Copy

DTI = (Total Monthly Debt Payments / Gross Monthly Income) × 100

Debt-to-Income (DTI) Calculator

The Impact of Debt on Credit Scores

- High credit utilization (>30%) lowers your score.

- Missed payments stay on your report for 7 years.

- Collections and defaults severely damage credit.

Debt Repayment Strategies

Managing debt effectively requires more than just determination—it demands a strategic approach tailored to your financial situation and goals. Among the most popular methods are the Debt Snowball Method , Debt Avalanche Method , Debt Consolidation , and Balance Transfers . Each offers unique benefits depending on your priorities, whether it’s staying motivated, minimizing costs, or simplifying payments.

Debt Snowball Method

The Debt Snowball Method focuses on paying off the smallest debts first while maintaining minimum payments on larger balances. Once the smallest debt is eliminated, the freed-up funds are redirected to the next smallest debt, creating a "snowball" effect. This method is particularly effective for those who need psychological motivation, as the quick wins of eliminating smaller debts provide a sense of accomplishment and momentum. For instance, someone with multiple credit card balances might start by paying off a 500debt,thenmoveontoa1,000 balance, gradually building confidence and discipline.

- Pay off the smallest debts first for quick wins.

- Motivational but may cost more in interest.

Debt Avalanche Method

In contrast, the Debt Avalanche Method prioritizes debts with the highest interest rates first, regardless of their size. By tackling high-interest debts early, this approach minimizes the total interest paid over time, resulting in significant cost savings. For example, if you have a credit card with a 25% APR and a personal loan at 10%, focusing on the credit card first reduces the compounding interest burden. While this method requires patience and discipline, it is ideal for individuals seeking the most financially efficient path to becoming debt-free.

- Prioritize high-interest debts to save money.

- More cost-effective but requires discipline.

Debt Consolidation

For those overwhelmed by multiple payments, Debt Consolidation offers a streamlined solution by combining all debts into a single monthly payment. This can be achieved through a personal loan or a balance transfer credit card. Consolidation simplifies budgeting and may lower your overall interest rate, making repayment more manageable.

- Combines multiple debts into one lower-interest loan.

- Best for those with good credit.

Balance Transfers

Similarly, Balance Transfers allow you to transfer high-interest credit card balances to a new card offering a 0% APR introductory period, typically lasting 12 to 18 months. During this time, all payments go directly toward reducing the principal, accelerating debt elimination. However, it’s crucial to pay off the balance before the promotional period ends to avoid reverting to high interest rates.

- Move high-interest credit card debt to a 0% APR card.

- Requires paying off the balance before the promotional period ends.

Budgeting to Pay Off Debt Faster

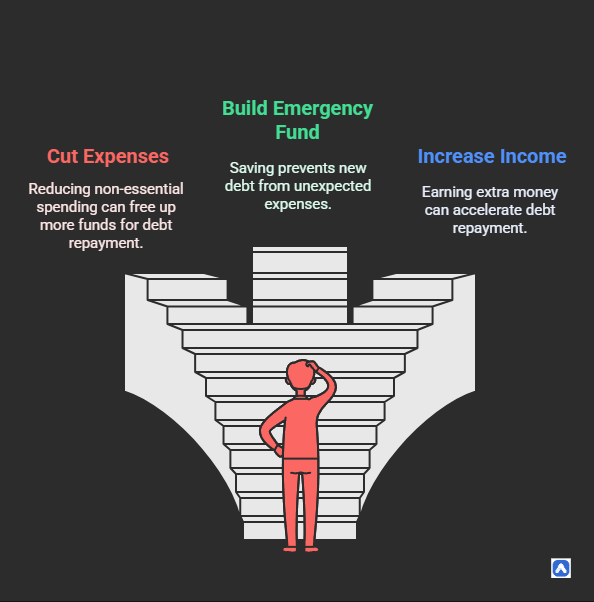

Creating and adhering to a budget is one of the most effective ways to accelerate debt repayment. A well-structured budget not only ensures that you allocate sufficient funds toward your debts but also helps you identify areas where expenses can be trimmed and income increased. To prioritize debt repayment, start by listing all your monthly expenses and categorizing them into essentials (e.g., housing, utilities, groceries) and non-essentials (e.g., dining out, entertainment). Then, allocate as much of your remaining income as possible toward your debt obligations. Tools like debt repayment calculators can help you project how extra payments will shorten your repayment timeline and reduce interest costs, keeping you motivated and on track.

Adjusting Your Budget

- Cut unnecessary expenses (subscriptions, dining out).

- Allocate extra funds to debt repayment.

Building an Emergency Fund

- Save $1,000 initially, then 3-6 months’ expenses.

- Prevents new debt from emergencies.

Increasing Income

- Side hustles (freelancing, gig economy jobs).

- Selling unused items.

Negotiating and Refinancing Debt

When dealing with overwhelming debt, negotiating with creditors and exploring refinancing options can significantly ease the burden. Preparation is key—gather documentation of your income, expenses, and repayment history to present a compelling case. Persistent yet respectful communication can yield favorable results, ultimately reducing the overall cost of your debt.

Lowering Interest Rates

One of the first steps is to negotiate lower interest rates with lenders. Many creditors are willing to adjust terms for borrowers who demonstrate a genuine commitment to repayment. For instance, contacting your credit card issuer and explaining your financial hardship may lead to a temporary reduction in interest rates or waived late fees.

- Call creditors to request rate reductions.

Debt Settlement

Another option to consider is debt settlement , where you negotiate with creditors to accept a reduced lump-sum payment in exchange for forgiving the remaining balance. While this can provide immediate relief, it comes with notable drawbacks. Debt settlement often damages your credit score and may result in taxable income on the forgiven amount. Additionally, some creditors may refuse to settle, leaving you with unresolved obligations. It’s crucial to weigh the pros and cons carefully and ensure you have the means to meet settlement terms before pursuing this route.

- Negotiate to pay less than owed (hurts credit).

Loan Refinancing

Refinancing existing debt through loan refinancing is another viable strategy, particularly when interest rates have dropped or your credit score has improved since the original loan was issued. Refinancing replaces your current debt with a new loan featuring better terms, such as a lower interest rate or extended repayment period. For example, refinancing a high-interest personal loan into a lower-rate installment loan can reduce monthly payments and total interest paid. However, it’s essential to account for any fees associated with refinancing, as they may offset potential savings.

- Replace high-interest loans with lower-rate options.

Dealing with Debt Collectors

Understanding your rights under the Fair Debt Collection Practices Act (FDCPA) is equally important when navigating debt negotiations. The FDCPA protects consumers from abusive practices by third-party debt collectors, such as harassment, false statements, or unfair collection tactics. Familiarize yourself with these rights to ensure fair treatment during interactions with creditors or collection agencies. By leveraging negotiation, refinancing, and legal protections, you can take control of your debt and work toward a more manageable financial future.

- Know your rights under the Fair Debt Collection Practices Act (FDCPA).

Debt Management Plans (DMPs) and Credit Counseling

For individuals struggling to manage overwhelming debt, enrolling in a Debt Management Plan (DMP) through a reputable credit counseling agency can provide structured guidance and relief. This approach simplifies budgeting and ensures consistent progress toward becoming debt-free.

What is a Debt Management Plan (DMP)?

A DMP is a formal agreement between you and your creditors, facilitated by a credit counselor, to consolidate unsecured debts into a single monthly payment. The counselor negotiates with creditors to lower interest rates, waive fees, and establish a realistic repayment schedule, typically spanning three to five years.

- A structured repayment plan through a credit counseling agency.

- Creditors may lower interest rates or waive fees.

Choosing a Reputable Credit Counseling Agency

Choosing the right credit counseling agency is crucial to the success of a DMP. Look for organizations accredited by trusted bodies like the National Foundation for Credit Counseling (NFCC) or the Financial Counseling Association of America (FCAA). Reputable agencies offer free initial consultations, transparent fee structures, and personalized advice tailored to your financial situation. Avoid companies that promise quick fixes or demand upfront fees, as these are often red flags for scams. Research reviews and verify credentials to ensure you’re working with a trustworthy partner in your debt management journey.

- Look for nonprofit agencies (e.g., NFCC, Money Management International).

- Avoid scams—check BBB and CFPB reviews.

Benefits of Debt Management Companies

Enrolling in a DMP through a debt management company offers several benefits, including reduced stress, simplified payments, and potential savings on interest. Programs like Trinity Debt Management specialize in creating customized plans that align with your income and financial goals, providing ongoing support throughout the repayment process.

- Single monthly payment.

- Reduced interest rates.

Risks to Watch For

- Fees (some agencies charge high costs).

- Not all creditors participate in DMPs.

Avoiding Debt Traps

One of the most insidious threats to financial stability is falling prey to common debt traps , many of which are designed to exploit vulnerabilities and perpetuate cycles of borrowing. Among the most notorious are payday loans and high-interest credit cards . Payday loans, marketed as short-term solutions for cash flow problems, often carry exorbitant annual percentage rates (APRs) exceeding 300%. Borrowers who cannot repay the loan by their next paycheck frequently roll it over, incurring additional fees that compound the debt. Similarly, high-interest credit cards lure users with initial low or zero-interest promotions, only to impose steep rates once the promotional period ends. These products disproportionately target individuals with limited financial literacy, trapping them in a cycle of escalating debt.

Common Traps

- Payday loans (400%+ APR).

- High-interest credit cards.

- Buy-now-pay-later schemes.

Predatory Lending Signs

Recognizing predatory lending practices is a critical step in protecting yourself from financial harm. Predatory lenders often employ aggressive marketing tactics, misleading terms, or hidden fees to ensnare borrowers. Warning signs include excessively high interest rates, mandatory arbitration clauses that limit legal recourse, and pressure to sign documents without adequate time to review them.

- No credit check required.

- Unclear terms.

- Pressure to sign immediately.

Smart Borrowing Habits

Building smart borrowing habits is the cornerstone of avoiding future debt problems. Before taking on any new debt, evaluate whether the purchase or investment aligns with your long-term financial goals.

- Only borrow what you can repay.

- Read contracts carefully.

Building Long-Term Financial Stability

Achieving debt freedom is a monumental milestone, but it’s only the beginning of a journey toward sustained financial health. After successfully repaying debts, the next step is to rebuild your credit score , which may have been impacted by past financial challenges. Start by maintaining a mix of credit accounts, such as a low-limit credit card or an installment loan, and consistently making timely payments.

Rebuilding Credit

- Pay bills on time.

- Keep credit utilization low.

Saving and Investing

- Contribute to retirement accounts.

- Build wealth beyond debt repayment.

Staying Debt-Free

- Stick to a budget.

- Avoid unnecessary loans.

Resources and Tools

Navigating the complexities of debt management becomes significantly easier with the right tools and resources at your disposal. For starters, debt repayment calculators are invaluable for planning and tracking your progress. These tools allow you to input details like your outstanding balances, interest rates, and monthly payments to simulate different repayment strategies. By comparing the Debt Snowball Method and the Debt Avalanche Method , you can determine which approach aligns best with your financial goals and timeline. Popular calculators, such as those offered by Bankrate or NerdWallet, provide detailed breakdowns and visualizations, empowering you to make data-driven decisions.

Best Debt Repayment Calculators

These tools help you create a strategy to pay off your debt efficiently and take advantage in debt management:

- Undebt.it : A free and customizable debt payoff planner that supports multiple repayment strategies, including the snowball and avalanche methods.

- NerdWallet’s Debt Calculator :A simple yet effective tool that helps you estimate how long it will take to pay off your debt based on different payment scenarios.

Recommended Budgeting Apps

Managing your budget is key to staying out of debt. These apps can help:

- YNAB (You Need a Budget) : A proactive budgeting app that encourages users to give every dollar a job and focus on future financial goals.

- Mint : A free app that tracks your spending, helps you set budgets, and provides insights into your financial habits.

Where to Find Financial Advice

If you need professional financial guidance, these organizations can help:

- NFCC.org (National Foundation for Credit Counseling) : A trusted nonprofit that offers credit counseling, debt management plans, and financial education.

- CFPB.gov (Consumer Financial Protection Bureau) : A government agency that provides resources on credit, debt, and financial rights.

Books & Podcasts

- The Total Money Makeover by Dave Ramsey

- The Dave Ramsey Show (podcast)

Final Thoughts

Debt management is not just about repaying what you owe—it’s about reclaiming control over your financial future. By implementing strategies like the Debt Snowball Method , Debt Avalanche Method , or enrolling in a structured Debt Management Plan (DMP) , you can systematically reduce your liabilities while minimizing costs. Pairing these approaches with tools like debt repayment calculators and budgeting apps ensures you stay organized and motivated throughout your journey.

Equally important is avoiding common pitfalls, such as falling into the trap of predatory lending or neglecting to build an emergency fund. By fostering smart borrowing habits and leveraging resources like credit counseling and financial education , you can prevent future debt issues and build a foundation for long-term stability. Organizations like Trinity Debt Management and government-backed programs offer invaluable support, guiding you toward sustainable solutions tailored to your needs.

Ultimately, mastering debt management empowers you to break free from financial stress and unlock opportunities for growth. Whether you’re rebuilding credit, saving for the future, or investing in wealth creation, the principles of disciplined budgeting and informed decision-making remain central to your success. Take the first step today—assess your debt, explore your options, and commit to a plan that aligns with your goals. With the right tools, strategies, and mindset, achieving financial freedom is not just a possibility but an attainable reality.

FAQS

How does debt management work?

Debt management works by consolidating debts, negotiating lower interest rates, and creating a repayment plan that fits your budget. This process is often facilitated by credit counseling agencies or debt management companies like Trinity Debt Management .

What is a debt management plan (DMP)?

A debt management plan (DMP) is a formal agreement between you and your creditors, typically managed by a credit counseling agency. It consolidates unsecured debts into a single monthly payment with reduced interest rates and fees.

How do I choose the best debt management plan for me?

To choose the best debt management plan , evaluate your financial situation, compare options from reputable debt management companies , and ensure the plan aligns with your ability to make consistent payments. Look for accredited organizations like Trinity Debt Management .

Can a debt management plan hurt my credit score?

Initially, enrolling in a debt management plan may slightly lower your credit score because creditors may close your accounts. However, consistent payments and reduced debt balances can improve your score over time.

What should I look for in a debt management company?

When choosing a debt management company , look for accreditation, transparency, positive customer reviews, and clear fee structures. Reputable companies like Trinity Debt Management are accredited by organizations such as the NFCC or FCAA.

What steps can I take to rebuild my credit after debt management?

After completing a debt management plan , focus on making timely payments, keeping credit utilization low, and maintaining a mix of credit accounts. Regularly monitor your credit report for errors and address them promptly.